Download

1 / 3

30 likes | 36 Views

How Banks And Credit Unions Make Money

E N D

How Banks And Credit Unions Make Money In this carefully slanted money related market, where every buyer is all around educated pretty much all the monetary occasions and news over the world, it isn't remarkable to think about how a bank increases its riches when it has fewer stores and a greater amount of withdrawals. It is very dumbfounding to know and translate the lucrative techniques that different banks and credit associations use to create cash. To rearrange it, how about we comprehend the straightforwardness behind the working of the banks by returning to the nuts and bolts of how banks and money related foundations work in the economy. Relatable: ‘’Revenue generation for banks’’ Banking is a great deal like some other business activities that individuals embrace. The main distinction being in the item that they attempt to purchase and sell for example cash. Banks get cash from their clients and loan that cash to those clients who need it. They additionally sell other monetary items like Certificate Of Deposits (CD), contract advances, vehicle advances, and house credits.

The absolute most normal courses through which banks procure their cash are: Loan cost Have you at any point asked why banks charge higher paces of premium when they advance out cash instead of giving enthusiasm on the cash stored by their clients? While the fundamental purpose behind this inconsistency is the hazard consider included giving out advances as banks have no sign when and if their advances would be forked over the required funds, this distinction in loan costs is likewise the essential wellspring of salary for banks. Speculations Banks don't simply contribute cash by loaning credits to their clients yet additionally put cash in land, organizations, and government protections. They additionally utilize the stores to exchange values, remote trade and the product advertised. On the off chance that the profits are ideal, they go about as a method of more benefits and incomes for the bank. Administration Fees Close by loaning and getting, banks likewise offer different administrations to their clients. They charge yearly expenses from credit and check card clients, ATM gets to, late installment punishments on advances, charges on dormancy of your record and furthermore charges on paper proclamations. Money related Advising Services Banks likewise give budgetary encouraging administrations to its clients who need to realize the most ideal approaches to contribute and develop their cash, however, this includes some significant downfalls as well! On the off chance that organizations need any assistance with respect to the issue of offers, the issue rate or data about any open contributions, the banks consistently stretch out their assistance to industrious clients. Interbank Lending On occasion, when a specific bank is lacking in furnishing its clients with the cash they need, they acquire from different banks to keep up their liquidity. For this reason, banks loan different banks cash yet at a particular pace of premium. This premium straightforwardly goes into the income pockets of banks. Along these lines, banks also help different banks in profiting.

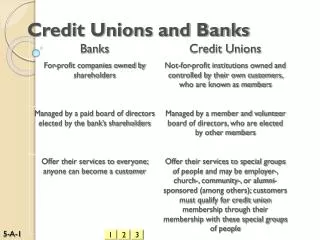

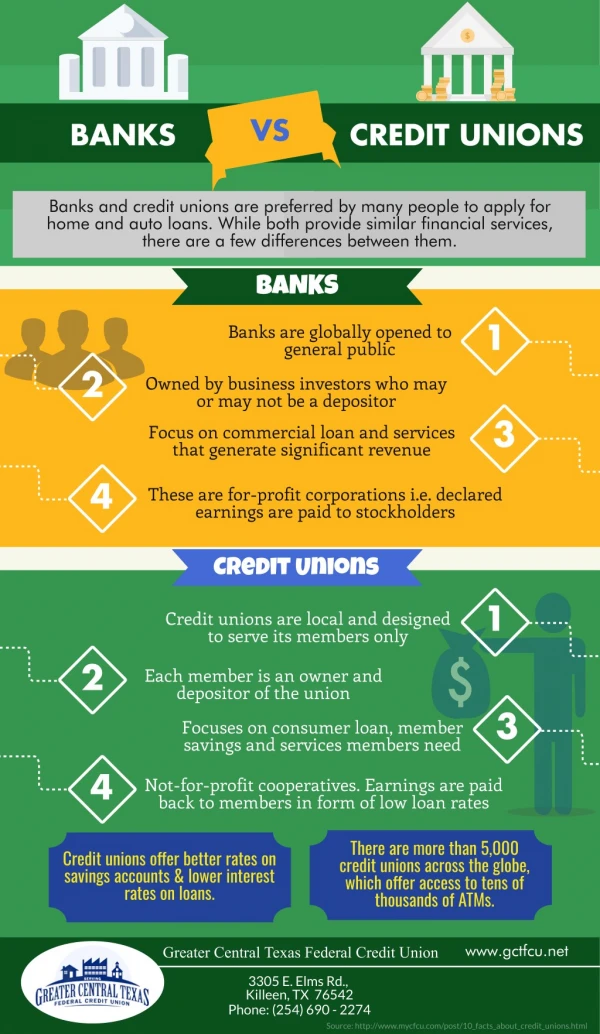

Credit Unions work similarly as banks and create income despite the fact that they are known to be non-benefit associations. What varies in their point of view is the way that credit associations charge higher pace of premiums on advances yet have lower expenses than banks as, despite the fact that their definitive rationale isn't expanded benefits, they do acquire some income out of it. They utilize their overabundance benefits for the correct working of the association or disseminate it among the individuals from the association. Rest, every one of their administrations and benefit age plans is like banks, which help them gain for their supportability.