Download

1 / 19

190 likes | 269 Views

CASE 02: SAIGON COOPMART<br>Logistics & Supply Chain plays an important role, if needed to say a critical factor for the success of Saigon Coopmart. Most of supermarkets over the world follow the identical model in which a warehouse is placed next to supermarket for stocks storage; and the size of warehouse is more or less equal to size of supermarket. However, due to harsh competition, and weak finance, Saigon Coopmart decided to follow a different model with very small size warehouse. This allows Saigon Coopmart to place more supermarkets; but in exchange, stocks only enough for a day, or maximum two compared to ordinary model in which a warehouse can store enough stocks for a week or more. As a consequence, Saigon Coopmart has to ship much more frequency to its supermarkets than its competitors such as Big C.<br> Gaining trusted in customers over years, sale increased gradually. In late 2011, Logistics and Supply Chain department received warning from some directors of Coopmart supermarkets (Saigon Coopmart has many supermarkets, each supermarket is supervised by one director) that they suspected by the end of 2012, the warehouse would no longer enough for a day sale. This means supermarket would not have enough products to sell for customer. A logistics improvement project was conducted to solve the problem temporary to spare time for BOD of Saigon Coopmart to come with a new and complete solution. One of the sub-projects involved improving the unloading time (i.e. when trucks carrying products come to supermarket, the products are then unloaded and moved to warehouse).<br>

E N D

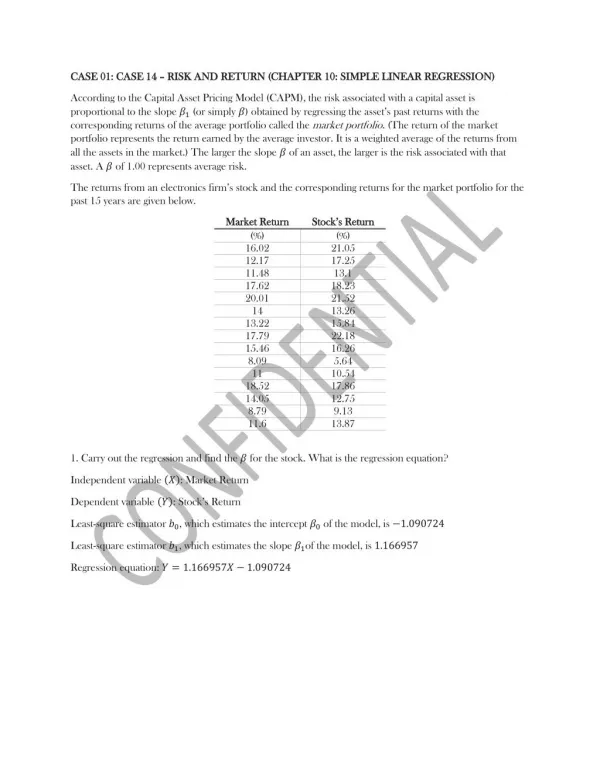

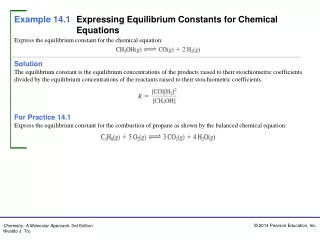

CASE 01: CASE 14 CASE 01: CASE 14 – – RISK AND RETURN (CHAPTER 10: SIMPLE LINEAR REGRESSION) RISK AND RETURN (CHAPTER 10: SIMPLE LINEAR REGRESSION) According to the Capital Asset Pricing Model (CAPM), the risk associated with a capital asset is proportional to the slope ?1 (or simply ?) obtained by regressing the asset’s past returns with the corresponding returns of the average portfolio called the market portfolio. (The return of the market portfolio represents the return earned by the average investor. It is a weighted average of the returns from all the assets in the market.) The larger the slope ? of an asset, the larger is the risk associated with that asset. A ? of 1.00 represents average risk. The returns from an electronics firm’s stock and the corresponding returns for the market portfolio for the past 15 years are given below. Market Return Market Return (%) 16.02 12.17 11.48 17.62 20.01 14 13.22 17.79 15.46 8.09 11 18.52 14.05 8.79 11.6 Stock’s Return Stock’s Return (%) 21.05 17.25 13.1 18.23 21.52 13.26 15.84 22.18 16.26 5.64 10.54 17.86 12.75 9.13 13.87 1. Carry out the regression and find the ? for the stock. What is the regression equation? Independent variable (?): Market Return Dependent variable (?): Stock’s Return Least-square estimator ?0, which estimates the intercept ?0 of the model, is −1.090724 Least-square estimator ?1, which estimates the slope ?1of the model, is 1.166957 Regression equation: ? = 1.166957? − 1.090724

y = 1.167x - 1.0907 25 20 15 Y 10 5 0 0 5 10 15 20 25 X Simple Regression CASE 14: Risk and Return r2 0.7775 0.8818 Coefficient of Determination Coefficient of Correlation Stock's Return Market's Return X 16.02 12.17 11.48 17.62 20.01 14 13.22 17.79 15.46 8.09 11 18.52 14.05 8.79 11.6 r Y Error 3.44607 4.13886 0.79406 -1.2411 -0.7401 -1.9867 1.50356 2.51056 -0.6904 -2.7099 -1.1958 -2.6613 -2.555 -0.0368 1.42403 Confidence Interval for Slope 1-a 1-a 95% 1.16696 (1-a a) C.I. for b b1 + or - 1 2 3 4 5 6 7 8 9 21.05 17.25 13.1 18.23 21.52 13.26 15.84 22.18 16.26 5.64 10.55 17.86 12.75 9.13 13.87 s(b1) 0.37405 0.17314 Standard Error of Slope 6.73986 0.0000 t p-value Confidence Interval for Intercept 1-a 1-a (1-a a) C.I. for b b0 95% -1.0907 + or - 5.38802 s(b0) 2.49403 Standard Error of Intercept Prediction Interval for Y 1-a 1-a X 95% 10 (1-a a) C.I. for Y given X 10.5788 + or - 10 11 12 13 14 15 5.35692 s 2.30593 Standard Error of prediction Prediction Interval for E[Y|X] 1-a 1-a X 95% 10 (1-a a) C.I. for E[Y | X] 10.5788 + or - 1.96969 ANOVA Table Source Regn. 241.543 Error Total 310.667 p-value 0.0000 F Fcritical 4.66719 SS df 1 13 14 MS 241.543 5.3173 45.4257 69.125

2. State your interpretation about the slope ?1 of the model (Hint: Does the value of the slope indicate that the stock has above-average risk? For the purposes of this case assume that the risk is average if the slope is in the range 1 ± 0.1, below average if it is less than 0.9, and above average if it is more than 1.1.) Since the least-square estimator ?1, which estimates the slope ?1of the model, is 1.166957 (> 1.10), the value of the slope indicate that the stock has above-average risk. 3. Give a 95% confidence interval for this ?. Can we say the risk is above average with 95% confidence? Confidence Intervals for the Regression Parameters: A (1 − ?)100% confidence interval for ?1is: ?1± ?(? 2,?−2)?(?1) A 95% confidence interval for ?1is: ?1± ?(0.025,15−2)?(?1) = 1.166957 ± (2.16)(0.17314) = [0.79291,1.54101] 4. If the market portfolio return for the current year is 10%, what is the stock’s return predicted by the regression equation? Give a 95% confidence interval for this prediction. If the market portfolio return for the current year is 10% (? = 10), the stock’s return predicted by the regression equation: ?̂= 1.166957? − 1.090724 = 1.166957(10) − 1.090724 = 10.57884 Prediction Intervals A (1 − ?)100% prediction interval for ? is: ?+(? − ?̅)2 1 15+(10 − 13.988)2 177.3712 ? ̂ ± ??/2?√1 +1 = 10.57884 ± (2.16)(2.3059)√1 + ??? = [5.2219,15.9358] 5. Construct a residual plot. Do the residuals appear random? A Check for the Equality of Variance of the Errors One of the assumptions in the regression model is the equality of variance of the errors. One of several ways to test for the normality of the residuals is to use a residual plot of the residuals. The residual plot is constructed as follows.

Residual Plot: Residual Plot 5 4 3 2 Error 1 0 -1 -2 -3 -4 X The residuals appear random. A graph of the regression errors, the residuals, versus the independent variable X, will reveal whether the variance of the errors is constant. The variance of the residuals is indicated by the width of the scatter plot of the residuals as X increases. If the width of the scatter plot of the residuals either increases or decreases as X increases, then the assumption of constant variance is not met. This problem is called heteroscedasticity. heteroscedasticity. When heteroscedasticity exists, we cannot use the ordinary least squares method for estimating the regression and should use a more complex method, called generalized least squares. The above figure shows a residual plot in a good regression, with no heteroscedasticity that the residuals appear random. 6. Construct a normal probability plot. Do the residuals appear to be normally distributed? The Normal Probability Plot One of the assumptions in the regression model is that the errors are normally distributed. This assumption is necessary for calculating prediction intervals and for hypothesis tests about the regression. One of several ways to test for the normality of the residuals is to use a normal probability plot of the residuals. The normal probability plot is constructed as follows.

Normal Probability Plot: Normal Probability Plot of Residuals The residuals appear to be normally distributed. In this plot, the residual values are on the horizontal axis and the corresponding z values from the normal distribution are on the vertical axis. If the residuals are normal, then they should align themselves along the straight line that appears on the plot. To the extent the points deviate from this straight line, the residuals deviate from a normal distribution. It is useful to recognize whether the assumption of normally distributed errors holds on a normal probability plot. The above figure a case where the residuals are relatively normal, but from the pattern of the points we can also infer that the distribution of the residuals is flatter than the normal distribution. 7. (Optional) The risk-free rate of return is the rate associated with an investment that has no risk at all, such as lending money to the government. Assume that for the current year the risk-free rate is 6%. According to the CAPM, when the return from the market portfolio is equal to the risk-free rate, the return from every asset must also be equal to the risk-free rate. In other words, if the market portfolio return is 6%, then the stock’s return should also be 6%. It implies that the regression line must pass through the point (6, 6). Repeat the regression forcing this constraint. Comment on the risk based on the new regression equation. The Excel Solver Method for Regression The Solver macro available in Excel can also be used to conduct a simple linear regression. The advantage of using this method is that additional constraints can be imposed on the slope and the intercept. For instance, if we want the intercept to be a particular value, or if we want to force the regression line to go through a desired point, we can do that by imposing appropriate constraints. As the given problem, consider a common type of regression carried out in the area of finance. The risk of a stock (or any capital asset) is measured by regressing its returns against the market return (which is the average return from all the assets in the market) during the same period. The Capital Asset Pricing Model (CAPM) stipulates that when the market return equals the risk-free interest rate (such as the interest rate of short-term Treasury bills), the stock will also return the same amount. In other words, if the market return risk-free interest rate 6%, then the stock’s return, according to the CAPM, will also be 6%. This means that according to the CAPM, the regression line must pass through the point (6, 6). This can be imposed as a

constraint in the Solver method of regression. Note that forcing a regression line through the origin, (0, 0), is the same as forcing the intercept to equal zero, and forcing the line through the point (0, 5) is the same as forcing the intercept to equal 5. The criterion for the line of best fit by the Solver method is still the same as before—minimize the sum of squared errors (SSE). Regression Using the Solver CASE 14: Risk and Return SSE 69.1435 Error 3.4513 4.1079 0.7566 -1.2208 -0.6974 -2.0005 1.4824 2.5324 -0.6905 -2.7793 -1.2378 -2.6326 -2.5683 -0.0996 1.3877 Intercept b0 -0.945353 1.157559 Slope b1 Prediction X 6 Y 6 X Y 1 2 3 4 5 6 7 8 9 16.02 12.17 11.48 17.62 20.01 14 13.22 17.79 15.46 8.09 11 18.52 14.05 8.79 11.6 21.05 17.25 13.1 18.23 21.52 13.26 15.84 22.18 16.26 5.64 10.55 17.86 12.75 9.13 13.87 25 20 15 10 11 12 13 14 15 Y 10 5 0 0 5 10 15 20 25 X Without any constraint, the regression equation is ?̂= 1.166957? − 1.090724 (obtained from the template for regular regression). For the market portfolio return of 6%, the predicted return of stock is ?̂= 1.166957? − 1.090724 = 1.166957(6) − 1.090724 = 5.911006 With the constraint, the regression equation changes as follows: Least-square estimator ?0, which estimates the intercept ?0 of the model, is −0.945353214 Least-square estimator ?1, which estimates the slope ?1of the model, is 1.157558869 Regression equation: ? = 1.157558869? − 0.945353214 Even though the risk of the regression model with the constraint (?1= 1.157558869) is lower than the risk of the original regression model without any constraint (?1= 1.166957958), the value of the slope still indicates that the stock has above-average risk.

CASE 02: SAIGON COOPMART CASE 02: SAIGON COOPMART Logistics & Supply Chain plays an important role, if needed to say a critical factor for the success of Saigon Coopmart. Most of supermarkets over the world follow the identical model in which a warehouse is placed next to supermarket for stocks storage; and the size of warehouse is more or less equal to size of supermarket. However, due to harsh competition, and weak finance, Saigon Coopmart decided to follow a different model with very small size warehouse. This allows Saigon Coopmart to place more supermarkets; but in exchange, stocks only enough for a day, or maximum two compared to ordinary model in which a warehouse can store enough stocks for a week or more. As a consequence, Saigon Coopmart has to ship much more frequency to its supermarkets than its competitors such as Big C. Gaining trusted in customers over years, sale increased gradually. In late 2011, Logistics and Supply Chain department received warning from some directors of Coopmart supermarkets (Saigon Coopmart has many supermarkets, each supermarket is supervised by one director) that they suspected by the end of 2012, the warehouse would no longer enough for a day sale. This means supermarket would not have enough products to sell for customer. A logistics improvement project was conducted to solve the problem temporary to spare time for BOD of Saigon Coopmart to come with a new and complete solution. One of the sub-projects involved improving the unloading time (i.e. when trucks carrying products come to supermarket, the products are then unloaded and moved to warehouse). a. Indicator UWPM (Unloading Weight/minute) is used to measure the effectiveness of unloading product management. From information provide (Excel data file –Sheet “Case 01 (a-b) –Coopmart”, what can you tell about the unloading product management among four Coopmart supermarkets? (Important note: any statistics test used HAVE TO comply with explanation/argument why using that statistics test). ANOVA Test The required assumptions of ANOVA: 1. We assume independent random sampling from each of the r populations. 2. We assume that the r populations under study are normally distributed, with means ?? that may or may not be equal, but with equal variances ?2. The null and alternative hypotheses here are, ?0:???= ????= ????= ??? ?1:??? ??? ???? ?? ??? ????? ANOVA Table ANOVA UWPM Sum of Squares df Mean Square F Sig. Between Groups 205089.155 3 68363.052 482.568 141.665 .000 Within Groups 229702.540 476 479 Total 434791.695 As shown in the above table, the p-value is smaller than 0.05, we reject the null hypothesis. We may conclude that, based on the testing results and our assumptions, it is likely that the four supermarkets

studied are not equal in terms of average UWPM. Which supermarkets are more effective than others? This question will be answered when we return to the given problem in the next section. The method we will discuss here is the Tukey method of pairwise comparisons of the population means. The method is also called the HSD (honestly significant differences) test. This method allows us to compare every possible pair of means by using a single level of significance, say ? = 0.05 (or a single confidence coefficient, say, 1 − 0.05 = 0.95). The single level of significance applies to the entire set of pairwise comparisons. To compare the population mean vacationer responses for every pair of supermarkets, we use the following set of hypothesis tests: ?0:???= ???? ?1:???≠ ???? ?0:???= ??? ?1:???≠ ??? ?0:????= ??? ?1:????≠ ??? ?0:???= ???? ?1:???≠ ???? ?0:????= ???? ?1:????≠ ???? ?0:????= ??? ?1:????≠ ??? From these comparisons we determine that our data provide statistical evidence to conclude that ??? is different from ????; ??? is different from ????; ??? is different from ???; ???? is different from ????; and ???? is different from ???. There are no other statistically significant differences at ? = 0.05. b. Further investigation shows that measuring the effectiveness by mean value is not enough because there might be a case in which two or more supermarkets having the same mean (weight/minute) but with different variance. Then, the one with smaller variance turns out to be better. Construct the hypothesis testing for two population variances matrix as follow:

From the result in that matrix and the result in question a, what is your conclusion? The F Distribution and a Test for Equality of Two Population Variances We assume independent random sampling from the four populations in question. We also assume that the four populations are normally distributed. The possible hypotheses to be tested are the following: Comparison between two population variance matrix Cong Quynh Dinh Tien Hoang ?0:??? ?1:??? Ly Thuong Kiet ?0:??? ?1:??? ?0:???? ?1:???? Hung Vuong ?0:??? ?1:??? ?0:???? ?1:???? ?0:???? ?1:???? 2 2 2 2 2 2 2= ???? 2≠ ???? 2 2= ???? 2≠ ???? 2 = ???? 2 ≠ ???? 2 2= ??? 2≠ ??? 2 = ??? 2 ≠ ??? 2 = ??? 2 ≠ ??? Cong Quynh 2 2 2 Dinh Tien Hoang 2 Ly Thuong Kiet Hung Vuong (I) Coopmart (J) Coopmart Test Statistic Critical Sig. Coopmart Cong Quynh Coopmart Dinh Tien Hoang 1.93226 1.43485 .0003 Coopmart Ly Thuong Kiet 5.19545 1.43485 .0000 Coopmart Hung Vuong 1.02779 1.43485 .8814 Coopmart Dinh Tien Hoang Coopmart Cong Quynh 1.93226 1.43485 .0003 Coopmart Ly Thuong Kiet 2.64625 1.43485 .0000 Coopmart Hung Vuong 1.91024 1.43485 .0005 Coopmart Ly Thuong Kiet Coopmart Cong Quynh 5.19545 1.43485 .0000 Coopmart Dinh Tien Hoang 2.64625 1.43485 .0000 Coopmart Hung Vuong 5.05498 1.43485 .0000 Coopmart Hung Vuong Coopmart Cong Quynh 1.02779 1.43485 .8814 Coopmart Dinh Tien Hoang 1.91024 1.43485 .0005 Coopmart Ly Thuong Kiet 5.05498 1.43485 .0000

2 is From these comparisons we determine that our data provide statistical evidence to conclude that ??? different from ???? ; ??? ; ???? and ???? is different from ??? 2 2 is different from ???? 2. There are no other statistically significant differences at ? = 0.05. 2 2 2 2 2; is different from ???? ; ???? is different from ??? 2 c. (Data for question c is in sheet “Case 01 (c) –Coopmart”) To improve the unloading products management, indicator unloading weight per minute (UWPM) is selected. This means higher UWPM is better. To improve UWPM, project manager need to know what are factors that affects to UWPM. A sample of 240 times unloading products were recorded. It is suspected that UWPM has close relation to two key factors. The first factor is the number of workers. The second factors is year of experience. For the first factor, since different time the total weight unloading is different; hence an appropriate indicator is total of worker involved/total weight (WIPW). For example, if 3,400kg of products need to unload and the number of worker in the trial is 7, then WIPW is = 7/3,400 = 0.002051. For the second factor, the average number of year experience of a group of workers (AvgYr) is used as an indicator. Construct a regression (Reg 1) in which UWPM is dependent variable, WIPW and AvgYr are independent variables. What information that the project manager can withdraw from the regression (Reg 1) above. Descriptive Statistics Descriptive Statistics Mean Std. Deviation N UWPM 122.117 44.2590 240 WIPM .003960 .0017123 240 AvgYr 3.6669 1.64448 240 The constructed multiple regression model in which UWPM is dependent variable and WIPW and AvgYr are independent variables is given by ? = 11.299 + 16,886.185?1+ 11.985?2+ ? The estimated regression relationship is: ?̂= 11.299 + 16,886.185?1+ 11.985?2 F-Test Is there a relationship between the dependent variable ?of UWPM and any of the explanatory, independent variables, ?1 and ?2, of WIPM and AvgYr suggested by the regression equation under consideration?

A statistical hypothesis test for the existence of a linear relationship between ? and any of the ?1 and ?2 is: ?0:?1= ?2= 0 ?1:??? ??? ?ℎ? ?? (? = 1,2) ??? ???? ANOVAa Model Sum of Squares df Mean Square F Sig. .000b 1 Regression 278085.484 2 139042.742 173.363 802.030 Residual 190081.189 237 239 Total 468166.673 a. Dependent Variable: UWPM b. Predictors: (Constant), AvgYr, WIPM As shown in the above table, since the p-value is small, we reject the null hypothesis that both slope parameters ?1 and ?2 are zero, in favor of the alternative that the slope parameters are not both zero. There is statistical evidence to conclude that, based on the testing results and our assumptions, a linear regression relationship existing between UWPM and at least one of the independent variables, WIPM or AvgYr (or both), proposed in the regression model. Model Summary Model Summaryb Adjusted R Std. Error of the Model R R Square Square Estimate Durbin-Watson .771a 1 .594 .591 28.3201 1.978 a. Predictors: (Constant), AvgYr, WIPM b. Dependent Variable: UWPM In the above table, ?2= 0.594, which means that 59.4% of the variation in UWPM is explained by the combination of the two independent variables, WIPM and AvgYr. Adjusted ?2 is 0.591, which is very close to the unadjusted measure. We conclude that the regression model fits the data very well since a high percentage of the variation in UWPM is explained by WIPM and/or AvgYr Coefficients Hypothesis tests about individual regression slope parameters: ?0:?1= 0 ?1:?1≠ 0 ?0:?2= 0 ?1:?2≠ 0 (1) (2)

Unstandardized Standardized Collinearity Coefficients Coefficients Statistics Model B Std. Error Beta t Sig. Tolerance VIF 6.319 1.788 .075 1 (Constant) 11.299 WIPM 16886.185 1071.371 .653 15.761 .000 .997 1.003 AvgYr 11.985 1.116 .445 10.744 .000 .997 1.003 We start with the test for the significance of variable ?1 as a prediction variable of WIPM. The hypothesis test is ?0:?1= 0 versus ?1:?1≠ 0. As shown in the above table, since the p-value is small, we reject the null hypothesis that the slope parameter ?1 is zero. We therefore conclude that there is statistical evidence that the slope of ? with respect to ?1, the population parameter ?1, is not zero. Variable of WIPM is shown to have some explanatory power with respect to the dependent variable, UWPM. The hypothesis test for ?2 is ?0:?2= 0 versus ?1:?2≠ 0. This p-value, too, is small. We conclude that ?2 of AvgYr is also an important variable in the regression equation. Finally, we conclude that both independent variables, WIPM and AvgYr, have close relation to the dependent variable, UWPM that positively affects UWPM. Both slope parameters, ?1 and ?2, are positive, which means that, everything else staying constant, the dependent variable of UWPM increases on average as WIPM increases or AvgYr increases (or both). Residual Plots The above figure is a plot of the regression residuals against the dependent variable UWPM. As we examine this figure carefully, we see that the spread of the residuals increases as UWPM increases. Thus, the variance of the residuals is not constant. We have the situation called heteroscedasticity—a violation of the assumption of equal error variance.

The Normal Probability Plot The above figure is the normal probability plot of the residuals. The residuals lie along and less deviate from the diagonal lie in the plot, they less deviates from the normal distribution. In the figure, the deviations appear to be significant, so we conclude that the model assumption that the population errors ∈? are normally distributed with mean zero and standard deviation ? is valid. Multicollinearity Correlation Correlations UWPM WIPM AvgYr Pearson Correlation UWPM 1.000 .629 .410 WIPM .629 1.000 -.053 AvgYr .410 -.053 1.000 Sig. (1-tailed) UWPM . .000 .000 WIPM .000 . .205 AvgYr .000 .205 . N UWPM 240 240 240 WIPM 240 240 240 AvgYr 240 240 240 In the correlation matrix shown in the above figure, we see that the correlation between the independent variables, WIPM and AvgYr, are not high (−0.053). This means that the two variables do not represent the same direction in space. Being lowly correlated with each other, the two variables do not contain the same

information about the dependent variable and therefore not cause multicollinearity when both are in the regression equation. Variance inflation factor Collinearity Statistics Model Tolerance VIF 1 (Constant) WIPM .997 1.003 AvgYr .997 1.003 The above figure shows the output for the current regression problem which contains the VIF values in the last column. We note that the VIF for variables, WIPM and AvgYr, are not greater than 5 that does not indicate the degree of multicollinearity existing with respect to the independent variables. CASE 03: CASE 03: TON DUC THANG TON DUC THANG UNIVERSITY UNIVERSITY – – CONTINUOUS IMPROVEMENT IN CONTINUOUS IMPROVEMENT IN EDUCATION PROGRAM EDUCATION PROGRAM Continuous improvement in education program is always one of the top strategic priority of Ton Duc Thang University. Every period, TDT University always applies the new teaching methods for continuously improving education programs. Recently, there is a suspect that the students perform better in the experiment classes (the classes are applied the new teaching method) compared to the control classes (the classes are applied the old teaching method). a.Present the methodology on how much test that suspect (what is your argument and what is an appropriate Statistics tests and why); b.How do you conduct sample for Statistics test; c.Present the result of your Statistics test; d.What is your conclusion from Statistics test?. Data Experiment Class Test 1 63 71 87 66 63 70 63 84 Control Class Test 1 88 59 85 64 95 92 71 58 Experiment Class Test 1 62 77 87 63 73 90 84 64 Control Class Test 1 83 80 94 53 70 90 57 82 Students 1 2 3 4 5 6 7 8 Test 2 84 89 70 73 74 97 89 80 Test 2 71 91 79 79 91 89 85 90 Students 31 32 33 34 35 36 37 38 Test 2 82 77 69 76 95 72 75 77 Test 2 91 63 79 92 58 86 74 82

9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 84 63 62 68 84 90 86 69 87 60 64 67 64 86 88 67 66 83 89 68 81 71 86 77 74 75 98 75 96 76 89 74 81 86 72 69 94 89 73 80 94 66 87 76 62 93 80 89 65 67 76 81 85 85 87 86 86 85 77 85 90 72 70 60 60 74 69 76 80 85 93 61 84 77 75 83 68 91 92 97 60 61 84 93 92 79 67 63 39 40 41 42 43 44 45 46 47 48 49 50 51 52 53 54 55 56 57 58 59 60 85 86 66 83 61 81 60 72 60 87 65 71 74 60 90 68 67 77 79 64 90 67 98 78 86 70 90 70 85 83 90 68 78 81 69 78 85 84 90 95 67 82 92 90 65 54 68 73 71 86 90 80 55 81 94 95 60 90 66 74 83 77 53 80 67 60 66 83 74 66 97 93 80 75 70 96 82 78 63 98 61 90 74 77 93 98 61 95 Experiment Class Test 1 84 90 63 69 81 67 63 62 90 86 83 80 89 69 64 90 77 Control Class Test 1 75 85 78 54 73 71 92 88 78 57 82 92 61 81 73 85 53 Experiment Class Test 1 84 90 63 69 81 67 63 62 90 86 83 80 89 69 64 90 77 Control Class Test 1 75 85 78 54 73 71 92 88 78 57 82 92 61 81 73 85 53 Students 61 62 63 64 65 66 67 68 69 70 71 72 73 74 75 76 77 Test 2 93 87 90 72 66 80 74 78 74 80 96 72 89 69 72 83 85 Test 2 89 61 74 71 97 93 61 89 69 72 73 59 84 70 86 61 95 Students 61 62 63 64 65 66 67 68 69 70 71 72 73 74 75 76 77 Test 2 93 87 90 72 66 80 74 78 74 80 96 72 89 69 72 83 85 Test 2 89 61 74 71 97 93 61 89 69 72 73 59 84 70 86 61 95

78 79 80 81 82 83 84 85 86 87 88 89 90 86 60 84 66 85 86 83 75 67 88 65 82 89 75 75 94 77 71 86 71 87 87 70 80 74 66 54 85 78 73 91 91 72 67 77 94 68 80 94 93 92 84 70 65 98 90 91 98 98 62 90 84 78 79 80 81 82 83 84 85 86 87 88 89 90 86 60 84 66 85 86 83 75 67 88 65 82 89 75 75 94 77 71 86 71 87 87 70 80 74 66 54 85 78 73 91 91 72 67 77 94 68 80 94 93 92 84 70 65 98 90 91 98 98 62 90 84 Descriptive Statistics Descriptive Statistics N Mean Std. Deviation Test 1 (Experiment Class) 120 75.8000 10.01981 Test 2 (Experiment Class) 120 81.6833 8.78882 Test 1 (Control Class) 120 75.6167 12.51767 Test 2 (Control Class) 120 120 79.1833 11.91777 Valid N (listwise) Pair Samples Statistics Test 1 Ex. - Co. -25 12 2 2 -32 -22 -8 26 22 -30 -18 -21 19 Test 2 Ex. - Co. 13 -2 -9 -6 -17 8 4 -10 17 1 -6 -10 5 Test 1 Ex. - Co. -21 -3 -7 10 3 0 27 -18 20 32 -2 10 -10 Test 2 Ex. - Co. -9 14 -10 -16 37 -14 1 -5 32 -5 12 4 -7 Students 1 2 3 4 5 6 7 8 9 10 11 12 13 Students 31 32 33 34 35 36 37 38 39 40 41 42 43

14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 23 10 -12 2 -25 -23 -19 -22 1 11 -18 -24 11 19 8 21 -3 14 12 -1 14 -9 13 -5 -20 -28 34 28 -11 -13 2 -13 20 13 44 45 46 47 48 49 50 51 52 53 54 55 56 57 58 59 60 -5 -30 -8 5 6 -29 -24 14 -30 24 -6 -16 0 26 -16 23 7 -23 5 8 20 -28 -4 3 6 -20 24 -6 16 18 -26 -16 31 -5 Test 1 Ex. - Co. 9 5 -15 15 8 -4 -29 -26 12 29 1 -12 28 -12 -9 5 24 32 -25 6 -7 -6 -5 Test 2 Ex. - Co. 4 26 16 1 -31 -13 13 -11 5 8 23 13 5 -1 -14 22 -10 -18 -17 10 7 6 -12 Test 1 Ex. - Co. 4 8 19 25 -6 -12 1 9 15 13 14 -19 1 -1 -24 16 -6 30 32 -5 2 -28 4 Test 2 Ex. - Co. 16 0 12 -7 -13 22 32 -4 14 4 -11 9 10 22 17 1 22 17 14 22 -6 6 29 Students 61 62 63 64 65 66 67 68 69 70 71 72 73 74 75 76 77 78 79 80 81 82 83 Students 91 92 93 94 95 96 97 98 99 100 101 102 103 104 105 106 107 108 109 110 111 112 113

84 85 86 87 88 89 90 11 8 -10 -6 -3 2 -5 -19 -4 -11 -28 18 -16 -18 114 115 116 117 118 119 120 3 16 29 -10 -4 9 -3 -7 17 15 -4 1 -9 30 Descriptive Statistics Descriptive Statistics N Mean Std. Deviation Test 1 (Ex.-Co.) 120 .1833 16.85728 Test 2 (Ex.-Co.) 120 120 2.5000 15.53797 Valid N (listwise) For each test (Test 1 and Test 2), the hypothesis test involves two populations: the population of students who study in the experiment class and the population of students who study in the control class. We want to test the null hypothesis that the mean test score in both populations is equal versus the alternative hypothesis that the mean for the experiment-class students is greater. Using the same students for the tests and pairing their observations in an experiment-and-control (Ex.-Co.) way makes the test more precise than it would be without pairing. Under these circumstances, it is easy to see that the variable in which we are interested is the difference between the test score of the students who study in the experiment class and that of the students who study in the control class. The population parameter about which we want to draw an inference is the mean difference between the two populations. For Test 1, we denote the population parameter by ??.???? 1, the mean difference. This parameter is defined as ??.???? 1= ???.???? 1− ???.???? 1, where ???.???? 1 is the average test-1 score of the students who study in the experiment class and ???.???? 1 is the average test-1 score of the students who study in the control class. Our null and alternative hypotheses are, then, ?0:??.???? 1≤ 0 ?1:??.???? 1> 0 For Test 2, we denote the population parameter by ??.???? 2, the mean difference. This parameter is defined as ??.???? 2= ???.???? 2− ???.???? 2, where ???.???? 2 is the average test-2 score of the students who study in the experiment class and ???.???? 2 is the average test-2 score of the students who study in the control class. Our null and alternative hypotheses are, then, ?0:??.???? 2≤ 0 ?1:??.???? 2> 0 The only assumption we make when we use this test is that the populations of differences are normally distributed.

Paired Samples Test Paired Differences 95% Confidence Interval Std. of the Difference Std. Error Sig. Sig. Mean Deviation Mean Lower Upper t df (2-tailed) (R-tailed) Pair 1 Test 1 (Experiment Class) - .18333 16.85728 1.53885 3.23041 .119 119 .905 .453 - Test 1 (Control Class) 2.86375 Pair 2 Test 2 (Experiment Class) 2.50000 15.53797 1.41842 -.30861 5.30861 1.763 119 .081 .040 - Test 2 (Control Class) As shown in the above table, for Test 1 (Pair 1), since the p-value is greater than levels of α even larger than 0.10, we conclude that the test-1 scores of the students who study in the experiment class is not higher than that of the students who in the control class. However, for Test 2 (Pair 2), since the p-value is smaller than α level of 0.05, we conclude that the test-2 scores of the students who study in the experiment class is higher than that of the students who in the control class, but the testing result is not strongly significant that may change at different levels of α. ------ THE END ------