Download

1 / 6

60 likes | 64 Views

If you want to find out how refinancing your mortgage can benefit you, speak with a Mortgage professional here. Click Here For Todayu2019s Mortgage Interest Rates.

E N D

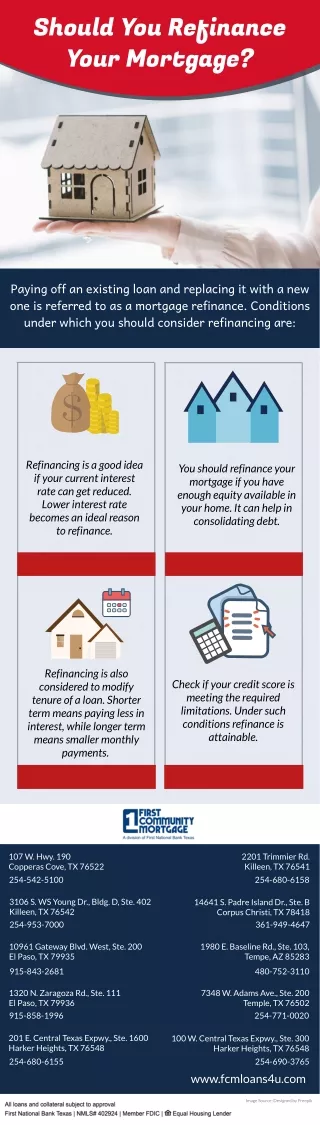

Get Started November 2019 6 Reasons Why You Should Re몭nance. Back to blog There are many reasons to consider re몭nancing your current Mortgage (and many of which can be to your bene몭t). We’ve created a list of some of the most common (and some of the best reasons) to Re몭nance. Lowering monthly payments Perhaps you’ve gone over your budget and realized you’d be more comfortable with paying less monthly. This is where Re몭nancing may get a chance to shine! By shopping around for a better Mortgage (weighing-out costs & rates) you can save big bucks monthly! There are different ways to save Re몭nancing: consolidating debt, obtaining a Lower Mortgage Interest Rate and/or APR or changing the term (timeframe) of the loan. When going over your options, it’s important to look-into the Equity in your home and your LTV (Loan-to-Value Ratio). If your Equity has gone-up you may be able to get a better Mortgage Interest Rate. Also, if you have more than 20% equity in your home, and you’re currently paying PMI (Private Mortgage Insurance) it’s possible to Re몭nance without the PMI. The “great” Mortgage Interest Rate on your ARM is about to expire

You got a “great” Mortgage Rate when you agreed to take out an adjustable-rate mortgage (ARM) but now the Rate is about to end; and with a 몭uctuating market, who knows if the change will be for the better, or for the worse. Before you get stuck paying more than you have to… shop around for a better Mortgage Interest Rate and, better yet, go for a 몭xed-rate loan. (You can get a much lower rate and keep that rate for the life of the Mortgage.) Your credit score went up! Congrats on the better score(s)! Now it’s time to get out there and compare. With better credit, you may qualify for a better mortgage rate on a brand new shiny Mortgage. This can equal less Monthly Mortgage Payments allowing the grip on your wallet to become a little looser. You can also improve your credit more; by lowering your monthly payments, it can make it easier for you to make payments thus furthering the positivity associated with your credit score. You need cash! Uh-oh… something’s come up and you need cash. The good news is that, if you have equity built-up in your home, you may be able to take cash out of your Equity. Here’s how it works… Let’s say you currently owe $200,000 on the mortgage but your home is worth $300,000- this means you have $100,000 in equity. But let’s say out of this $100,000 you only need $50,000 in cash. You can actually take $50,000 cash from your Equity. This means that the new Mortgage amount would be $250,000. By re몭nancing with a cash-out option, you can use the cash from your equity to pay off some of your Debts (that fancy wedding from a few years ago, credit cards, student loans, auto loans, etc.), or use that money for other situations (home improvements, home repairs, medical bills, auto repairs, etc.). Payoff your loan sooner with higher Monthly Payments Looking to get out of Debt sooner? There are a couple of ways to do this with a ReFi. One way is to make your Monthly Mortgage Payments higher in order to pay off the loan sooner, and also save money on Interest Payments. To do this, you may need to change the term of the loan; shortening the life of the loan. Or, you can speak to a Mortgage Lender about increasing the amount you’re currently paying back on your Monthly Mortgage Payments.

Consolidate your debt Want to make paying back your debts more streamlined (and possibly cheaper)? By re몭nancing to consolidate your debt, it’s entirely possible! By rolling all of your other debts (or at least some of your other debts) into your Mortgage, you can just pay one lump sum every month at the same Mortgage Interest Rate. This means if you’re able to shop around, and you 몭nd a better rate than what you’re currently paying back, you can save money monthly while also making getting out of debt easier on yourself. If you want to 몭nd out how re몭nancing your mortgage can bene몭t you, speak with a Mortgage professional here. Click Here For Today’s Mortgage Interest Rates. Financial Tips Share post: Re몭nancing Was this article helpful? Yes No 2 out of 2 found this helpful Related posts November 2019 December 2016 You’re Locked-in, But Don’t Worry… Tim Waller’s The NJ Real Estate Show Interviews Get A Rate’s Nick Marenoski Perhaps you’ve heard the term “Lock In” regarding

Mortgage Interest Rates. It sounds like a big, and pe... The NJ Real Estate Show, a weekly radio show hosted by real estate veteran Tim Waller, sat down with Get... Buying a Home Financial Tips Buying a Home Re몭nancing Financial Tips November 2019 November 2019 Your DTI When Re몭nancing… Let’s Prepare for a ReFi! Getting ready for a ReFi? Don't panic! Let us help you get prepared by looking over out Preparing for a ... So you’re about to Re몭nance your home- nice! There are many things to consider before moving forward. Most... Financial Tips Financial Tips Re몭nancing Tools Purchase Calculator Re몭nance Calculator Affordability Calculator Rent vs Buy Calculator Credits / Points Calculator Programs

Comparison 30 Years Fixed 15 Years Fixed FHA Loan VA Loan About Us Company Information Press Room Careers Testimonials Contact Learn Blog FAQs Of몭ces NJ Of몭ce FL Of몭ce GA Of몭ce CA Of몭ce © 2021. Get A Rate LLC. All Rights Reserved NMLS #907795 Licensed Residential Mortgage Lender in CA, WA, GA, TX, PA, CT, FL, SC, IL and NJ (by the NJ Department of Banking and Insurance). Equal Housing Opportunity Lender. When and if acting as a broker, Get A Rate will not make commitments or fund mortgage loans. Registered NY Mortgage Broker. All NY mortgage loans are arranged with third party lenders – Get A Rate LLC does not directly offer or guarantee NY interest rates or loan programs and does not directly issue commitments or make 몭nal decisions on loan terms. This website is not authorized by the NYDFS and that no applications can be taken for NY loans on the site. Get A Rate LLC is an FHA Approved Direct Lending Institution, and is not acting on behalf of or at the direction of HUD/FHA or the Federal government. These programs are not a commitment to lend and program guidelines are subject to change. Additional Disclosures Home / HUD & RESPA / State Licenses & Disclosures, Terms & Conditions, Privacy Policy / 888-562-2611 / Rate Lock Policy / NMLS Consumer Access