Download

1 / 21

220 likes | 503 Views

WORLD OIL PRICES Barry L. Evans Evans, Frey & Walker ______ SPE Los Angeles Basin Section Meeting, November 8, 2005 Long Beach, CA OUTLINE Oil Price History & Current Prices Factors Affecting Oil Prices Current Supply & Demand Twilight in the Desert? The Coming Oil Crunch

E N D

WORLD OIL PRICES Barry L. Evans Evans, Frey & Walker ______ SPE Los Angeles Basin Section Meeting, November 8, 2005 Long Beach, CA

OUTLINE • Oil Price History & Current Prices • Factors Affecting Oil Prices • Current Supply & Demand • Twilight in the Desert? • The Coming Oil Crunch • Summary

FACTORS AFFECTING OIL PRICES 1. Supply and Demand-Actual and perceived 2. Excess production capacity 3. Political events and /or political instability 4. Inventories and strategic storage 5. Weather, actual and expected 6. Speculative investment 7. Value of the dollar

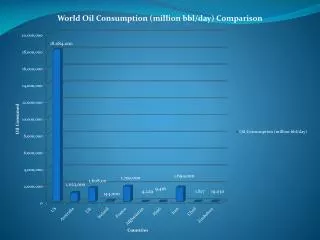

CURRENT SUPPLY & DEMAND 1. In every year since 1985 the world consumed more has oil than has been discovered. (Figure 2) 2. Spare capacity was 10MM bbls in 1987. Growth in non-OPEC oil production supplied increases in demand over past 20 years. OPEC countries lacked incentive to develop new production. 3. Non-OPEC oil is currently maxed out. Only OPEC (Saudi Arabia) has significant excess capacity. However, with the latest increases by OPEC it is now only about 1-2 MMB.

CURRENT SUPPLY & DEMAND 1. In every year since 1985 the world consumed more has oil than has been discovered. (Figure 2) 2. Spare capacity was 10MM bbls in 1987. Growth in non-OPEC oil production supplied increases in demand over past 20 years. OPEC countries lacked incentive to develop new production. 3. Non-OPEC oil is currently maxed out. Only OPEC (Saudi Arabia) has significant excess capacity. However, with the latest increases by OPEC it is now only about 1-2 MMB.

CURRENT SUPPLY & DEMAND 4. Future supply may not be able to match demand. This would have a major effect on the economies of the world. 5. Most analysts believe that a “cushion” of about 3% of demand is required to maintain a smooth global oil supply and avoid “price shocks”. At 2005 demand of 83.8 MMB/D this would be 2.5 MMB/D. 6.The increased income due to higher prices will encourage investment to develop new reserves. However, the lead time for major projects is 3-5 years.

CURRENT SUPPLY & DEMAND 1. 2004 demand was 82.1 MMB/D, an increase of 2.55MMB/D or 3.2% over 2003. The increase in China was 15%, India 10%, USA 3 %. 2. 2005 demand is estimated to be 2.1% over 2004, a gain of 1.7MMB/D. (Figure 3) 3. The current high oil prices with a strong possibility of even higher prices will lower demand and the level of economic activity. This will put pressure on prices.

CURRENT SUPPLY & DEMAND 1. 2004 demand was 82.1 MMB/D, an increase of 2.55MMB/D or 3.2% over 2003. The increase in China was 15%, India 10%, USA 3 %. 2. 2005 demand is estimated at 83.8MMB/D, 2.1% over 2004, a gain of 1.7MMB/D. Figure 3) 3. The current high oil prices will lower demand and the level of economic activity. This will put downward pressure on prices.

Matthew Simmon’s Concerns 1. 90% of oil production comes from 4 large mature oil fields. All are under waterdrive. Ghawar accounts for about 50% of oil production (5MMB/D). 2. Since 1982 OPEC countries have not published field by field production data. 3. Saudi Arabia has been extensively explored. 4. Saudi claims of 15 million B/D oil for 50 years cannot be verified.

Simmon’sConcerns (cont’d) 5. Large reserve increases in the past are largely unexplained. 6. Saudi Arabia oil production is vital to help meet the world’s rising demand. 7. Transparency of energy information from Saudi Arabia is critical for the world’s economic planning. 8. A third party estimate of Saudi reserves would be extremely valuable.

THE COMING “OIL CRUNCH” 1. Two basic schools of thought. The “economic“ group believes that higher prices will encourage more exploration and the additional oil needed to meet rising demand will be found. 2. The second group sees oil and gas as a “finite” quantity and are believers in the Hubbert’s “peak oil” theory.

THE COMING OIL CRUNCH (cont’d) 3. M. King Hubbert predicted in 1956 that USA oil production would peak in 1966-1972. It peaked in 1970 @ 9MMB/D. 4. Many oil analysts now use his basic method to estimate peak rates for oil fields and major supply areas. 5. John S. Herold Inc. has made current estimates of peak oil rates for 24 oil companies, e.g. ExxonMobil 2008, ChevTex 2009.

THE COMING OIL CRUNCH (cont’d) 6. Forecasts: Non-OPEC could peak 2005-2010. FSU, 2008-2014. There will be a growing dependence on OPEC. OPEC peak estimated 2025-2035 depending on demand and OPEC reserves. Forecasts vary depending upon the estimates of URR. 7. USA (25% world’s energy & 5% world population) needs to embark on a strong conservation program that will reduce demand on the world’s energy supply. 8. Critical need to recognize the situation and develop more non-conventional oil (tar sands, heavy oil, oil from oil shale and coal) and renewable sources such as more nuclear plants, solar and wind.

SUMMARY 1. There is a growing consensus, including oil companies, e. g. BP, that oil production will peak in the not too distant future. 2. The “oil age” , like the “wood age” and the “coal age” may be nearing an end. 3. If OPEC oil reserves are overstated, the oil “peak rate” for OPEC could come much sooner. 4. Due to the time required to develop other energy sources, a shortfall of energy supply could seriously affect world economies. 5. Without adequate energy sources the “industrial society” of the last 100-150 years is threatened. Conflicts for oil supplies are possible in the future.

SUMMARY (cont’d) 4. The world is currently on a “tightrope” due to supply and demand being about even, low inventories and a tanker shortage. 5. Oil prices can be expected to remain at high levels ($50-60/bbl WTI) until demand slows and additional supplies become available. Price volatility can be expected. 6. Oil prices can be expected to go much higher in 10-15 years as dependency on OPEC oil increases.