Download

1 / 29

290 likes | 719 Views

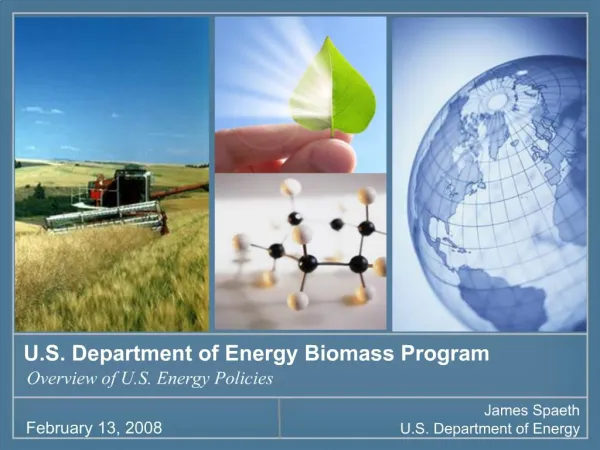

U.S. Department of Energy Biomass Program. Growing A Robust Biofuels Economy. Office of Biomass Program. June 2007 Corporate Presentation. 2005 Global Petroleum Product Consumption. 2005 Global Biofuel Production. 388 billion gallons/yr. 454 billion gallons/yr. 13 billion gallons.

E N D

U.S. Department of Energy Biomass Program Growing A Robust Biofuels Economy Office of Biomass Program June 2007 Corporate Presentation

2005 Global Petroleum Product Consumption 2005 Global Biofuel Production 388 billion gallons/yr 454 billion gallons/yr 13 billion gallons Total = 862 thousand barrels/day Total = 82.4 million barrels/day Sources: BP Statistical Review of World Energy; National Biodiesel Board, European Biodiesel Board, Renewable Fuels Association Navigant 2005 Biofuels Market Below 2% of Global Transportation Fuel Use

U.S. Presidential Commitment to Ambitious Biofuels Goals • Cost-competitive cellulosic ethanol” by 2012 • “20 in 10” • Reduce U.S. gasoline* use by 20% by 2017 through… • 15% reduction from new Alternative Fuels Standard at35 billion gallons/year • 5%reduction from enhanced efficiency standards (CAFÉ) • “30 in 30” • Longer-term DOE biofuels goal • Ramp up the production of biofuels to 60 billion gallons • Displace 30% of U.S. gasoline consumption* by 2030 * light-duty vehicles only

Biomass R&D Initiative (BRDI) • Multi-agency effort to coordinate and accelerate all Federal biobased products and bioenergy research and development. • Mandated under the Biomass Research & Development Act of 2000, further revised by Energy Policy Act of 2005 (Sec 937). • BRDI coordinating bodies • Biomass R&D Board, a cabinet level council co-chaired by DOE and USDA – also includes DOI, DOT, EPA, DOC. • Biomass R&D Technical Advisory Committee – 30 senior individuals from industry, academia, state government • Aims to deliver National Biofuels Action (NBA) Plan by Fall 2007. www.brdisolutions.com

How Do We Achieve These Goals? Three-pronged approach • Effective RD&D Program • Effective policies • Private sector investments Policy DOE Biomass Program RD&D/ Technology Market/Capital Investments

Biomass Program Mission Develop and transform our renewable and abundant biomass resources into cost competitive, high performance biofuels, bioproducts, and biopower. Collaborative R&D • Partnerships • Policy • Interagency Coordination Integrated Biorefineries: Systems Integration and Demonstration Core activities accelerate the technological advances needed to supporta domestic bioindustry producing cellulosic ethanol and other biofuels in integrated biorefineries.

Office of Biomass Budgets Biomass Program Budget FY2002-FY2008 Millions of Dollars The Advanced Energy Initiative and 20 in 10 have provided a boost in funding for biofuels in FY2007 and FY2008

“First generation” biofuels are commercially developed technologies, but have high costs and limited scalability… R&D Demo Market Entry Market Penetration Market Maturity Corn and Sugarcane Ethanol Cellulosic Ethanol Mixed OH; Fischer-Tropsch Rapeseed and Soy Biodiesel Renewable Diesel Butanol; DME • 1st Generation Biofuels • Ethanol is a clean burning, high-octane alcohol fuel used as a replacement and extender for gasoline • Has been commercially produced since the 70s in the US and Brazil, still the market leaders • Corn ethanol is cost competitive (with no subsidies) with gasoline when crude oil is above $50/barrel ($30/brl from sugar cane) • Biodiesel is a high-cetane, sulfur-free alternative to (or extender of) diesel fuel and heating oil • Commercialized in Europe in the 90’s • Worst economics (and smaller market) than ethanol • 2nd Generation Biofuels • R&D efforts are focused on: • Increasing the range of feedstock from which to produce biofuels • Reducing biomass-to-liquid conversion costs • Two main technology platforms in development: • Biochemical pathway: conversion of the cellulose to sugars and fermentation to alcohol fuels • Thermochemical pathway: gasification of biomass to syngas and synthesis to fuels • Commercial renewable diesel plants are under construction (e.g., Neste oil “NexBTL”) Second generation” technologies aim to resolve these limitations Source: Navigant

Targeted R,D &D: Overcoming Barriers Future efforts will address obstacles to biochemical and thermochemical routes to biofuels, support demonstrations, and resolve infrastructure issues. • Barriers • High cost of enzymatic conversion • Inadequate technology for producing ethanol from sugars derived from cellulosic biomass • Limitations of thermochemical conversion processes • Demonstration/integration of technology in biorefineries • Inadequate feedstock and distribution infrastructure • Solutions • R&D to improve effectiveness and reduce costs of enzymatic conversion • R&D on advanced micro-organismsfor fermentation of sugars • Re-establish thermochemical conversion as a second path to success • Fund loan guarantees, commercial biorefinery demonstrations, and 10% scale validation projects • Form interagency infrastructure and feedstock teams

Biomass Program Portfolio Removing barriers to large-scale production of cellulosic biofuels Collaborative R&D • Feedstocks: integration of feedstocks with conversion processes • Conversion Technologies: biochemical and thermochemical Integrated Biorefineries • Systems Integration: feedstocks, conversion, biopower, infrastructure • Demonstrations: pilot scale and commercial scale for diverse feedstocks Infrastructure (New) OBP organizes to deliver against barriers

Cellulosic Ethanol Growth $6.0 U.S. Ethanol Production $5.0 $4.0 Billion Gallons of Ethanol $3.0 2002 Dollars per Gallon/Ethanol $2.0 Cellulosic Corn $1.0 OBP RD&D Activities & Timeline Biorefinery Demos 10% Scale Validation Pre-Validation Integrated Biorefineries IBRF Commercial Ethanologen Adv. Feedstocks & Conversion Technology R&D 1st Generation Feedstock, Biochemical,Thermochemical Core R&D 11

Collaborative R&D Is Producing Results Achievements • Achieved substantial decrease in cost of ethanol production – from over $5 to approximately $2.26 per gallon • Developed organisms with superior ability to convert mixed sugars to ethanol – an important step toward cellulosic ethanol and the 2012 goal • Developed high-value plastics, foams, and coatings from oil crops and corn sugar Cell phone casings made from bio-based polymers developed through DOE-industry cost-shared R&D The program can already claim many successes

DOE Office of Science: Complementary Basic Research on Biomass • Invests $375 million to fund three new Bioenergy Research Centers to accelerate basic research on the development of cellulosic ethanol and other biofuels. • Recently issued a joint biofuels research agenda with the EERE Office of Energy Efficiency and Renewable Energy – Breaking the Biological Barriers to Cellulosic Ethanol. • Part of the NBA Plan effort

How Do We Achieve These Goals? Three-pronged approach • Effective RD&D Program • Effective policies • Private sector investments Policy DOE Biomass Program RD&D/ Technology Market/Capital Investments

Policy Drivers & Incentives Supporting Biofuels Examples of Policies • Energy Security/ Political Tensions • Resource Diversification • Petroleum Prices/Volatility Energy • United States • Energy Policy Act of 2005 (federal policy) • State tax credits, blend requirements… • Europe • Tax credits: most common incentive • EU set target for biofuels consumption (similar to RFS, but not a mandate) Asia • China, India, and Malaysia introducing policies to support biofuels • Japan has tax credits in place South America • Brazil: Ethanol blending requirements in place and a requirement for biodiesel starting in 2008 Environment • Climate Change • Air Pollution • Economic Development • Farm Income Agriculture • Ethanol is currently the most prevalent US biofuel Biofuels Source: Navigant Biofuels require a comprehensive & effective policy framework

Policies Accelerating Biofuels Production Energy Policy Act 2005 (EPAct 2005) • Section 932: Commercial Integrated Biorefinery • Secretary Bodman recently announced six awards • $53 million in FY 2007 budget request • Section 941: Revisions to Biomass R&D Act of 2000 • Vision document released November 2006; updated Roadmap due May 2007 • Section 942: Cellulosic Ethanol Reverse Auction • Request For Information and Options papers completed • $5 million requested for FY 2008 • Sections 1510, 1511, and Title XVII: Loan Guarantees • DOE issued guidelines for the first Loan Guarantees under Title XVII in August 2006 • Loans for conversion of Municipal Solid Waste and cellulosic biomass to fuel ethanol and other commercial byproducts also considered under this offering EPAct 2005 goals are integrated into core technology priorities.

New Policies May Foster Market Expansion • National strategy for low level blends/ Regional strategy for E-85 • RFS with greater requirements for cellulosic ethanol • Stronger incentives for all biofuels • Extension of ethanol subsidies to 2015 • Payments to lignocellulosic biomass suppliers for residues and energy crops • Tougher greenhouse gas regimes • State support – individual state mandates/ legislation Ramp-up of ethanol production will require innovative and focused policies for infrastructure and feedstocks

How Do We Achieve These Goals? Three-pronged approach • Effective RD&D Program • Effective policies • Private sector investments Policy DOE Biomass Program RD&D/ Technology Market/Capital Investments

The future of biofuels will depend on the creation of new partnerships among several industries Agribusiness Petroleum Industrial Biotech BANKING Forest Products Future Biorefineries Utilities Chemicals Source: Navigant

Global Ethanol Status 13% Increase • 2005 Production: 12,150 million gallons • 35% -- U.S. (corn) • 35% -- Brazil (sugarcane) • 8% -- China (feedstock unknown) • 22% -- Other Countries (wheat, barley, beet) • 2004 Production:10,770 million gallons Other China U.S. Brazil 2004 2005 The market is placing bets on biofuels

While biofuels represent only 3% of US transportation fuels today, production is growing rapidly. US Markets Driven by High Prices and RFS: Building Capacity U.S. Ethanol Production Capacity Capacity Under Construction: 6.14 Billion Gallons per Year Expected by End of 2008 Total Capacity with Current & New Construction: 11.7 billion gallons per year Billion Gallons Current Production Capacity: 5.58 Billion Gallons per Year *Estimated as of February 7, 2007. Source: Renewable Fuels Association.

Ethanol Plants Focused on Midwest; “Destination” Plants Increasing One of the drivers for destination ethanol plants is to produce DDGS closer to market. Source: Navigant

U.S. Ethanol Infrastructure FFV’s in Service (millions) Operating E85 Stations Industry Background Operating Plants Source: Alternative Fuels Data Center, March 8, 2007 78 As of 3/8/07 114 Source: Renewable Fuels Association As of 2/25/07 Existing infrastructure must expand & improve to meet future biofuels demand

DOE absorbs some of the risk through focused RD&D program Value vs. Time Technical & Market Risk vs Time HIGH RISK, LOW VALUE LOW RISK, HIGH VALUE Value of Investment Risk of Investment Operating Cellulosic Ethanol Facilities Demonstration Commercialization Applied R&D 2011: Operation of 932 and 10% Scale Facilities 2006: Loan Guarantee Program; Section 932 Demonstrations 2018: Genomics-Improved Feedstocks 2025: Integrated Ethanol/ Bioproduct Facilities RD&D Timeline 2012: Reduced Enzyme and Feedstock Costs ($1.31/gallon cost target) 2007: Ethanologen Solicitation 2014: Repeatable Plant Design Packages DOE focuses on investment risk reduction to drive market

Cellulosic Biorefinery Investments Recently announced competitive selections to provide up to $385 million over four years for cost-shared integrated biorefineries in six states • Abengoa Bioenergy Biomass of Kansas Capacity to produce 11.4 million gallons of ethanol annually using ~700 tons per day of corn stover, wheat straw, milo stubble, switchgrass, and other feedstocks • ALICO, Inc. Capacity to produce 13.9 million gallons of ethanol annually using ~770 tons per day of yard, wood, and vegetative wastes and eventually energy cane • BlueFire Ethanol, Inc. Sited on an existing landfill, with capacity toproduce 19 million gallons of ethanol annuallyusing ~700 tons per day of sorted green wasteand wood waste from landfills

Cellulosic Biorefinery Investments • Poet Capacity to produce 125 million gallons of ethanol annually (~25% will be cellulosic ethanol) using ~850 tons per day of corn fiber, cobs, and stalks • Iogen Biorefinery Partners, LLC Capacity to produce 18 million gallons of ethanol annually using ~700 tons per day of agricultural residues including wheat straw, barley straw, corn stover, switchgrass, and rice straw • Range Fuels (formerly Kergy Inc.) Capacity to produce 40 million gallons of ethanol annually and 9 million gallons per year of methanol, using ~1,200 tons per day of wood residues and wood based energy crops

Upcoming solicitations • 10% Validation Solicitation: Imminent announcement • One-tenth of the projected scale of a first of its kind commercial facility • Integrated biorefinery demonstrations using cellulosic feedstocks and producing a combination of fuels, chemicals, and substitutes for petroleum-based feedstocks and products • Enzyme Solicitation: FY07 • Second phase of cellulase development with cost-sharing industry partners • Create commercially available, highly effective & inexpensive enzyme systems for biomass hydrolysis • Thermochemical Conversion Solicitation: FY07 • Integration of gasification and catalyst development • Freedom Prize

Other ways to get involved • Advisory Committee (TAC): Seats renewed periodically • Comments to Biomass R&D Board, DOE, OBP, etc… • Participate in regional feedstock partnerships • Communicate benefits of cellulosic biofuels • Etc…all ideas are welcome

Contact Info • Office of Biomass Programs • Jacques Beaudry-Losique, 202-586-5188 • Web Site: http://www1.eere.energy.gov/biomass/ • Golden Field Office • Jim Spaeth, jim.spaeth@go.doe.gov • Office of Science • Sharlene Weatherwax, sharlene.weatherwax@science.doe.gov • USDA • Bill Hagy, bill.hagy@wdc.usda.gov • EERE INFO CENTER • http://www1.eere.energy.gov/informationcenter/ THANKS