Download

1 / 10

100 likes | 100 Views

DK Goel Solutions Class 11 Chapter 6 Accounting Equation as per latest DK Goel Accountancy Book available for free.<br><br>https://dkgoelsolutions.com/class-11/chapter-6-accounting-equations/

E N D

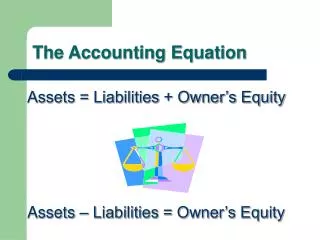

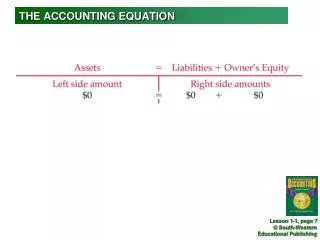

DK Goel Solutions Chapter 6 Accounting Equations DK Goel Accountancy Class 11 Solutions Chapter 6 Accounting Equations are made by master Accountancy instructors from the DK Goel Class 11 Accountancy books. We at DKGoelSolution'S give DK Goel Solutions to help student in building up a far reaching comprehension of the multitude of hypotheses. There are various ideas in Accountancy, yet the ideas of Trial Balance, Depreciation and Bank Reconciliation Statement (BRS) are quite possibly the most significant of all. DK Goel Accountancy Class 11 Solutions – Chapter 6 Short Question Question 1: Give two basic purposes of the accounting equation.

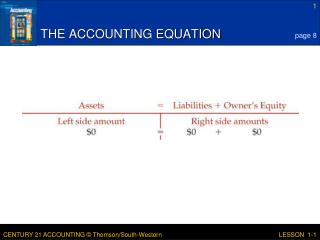

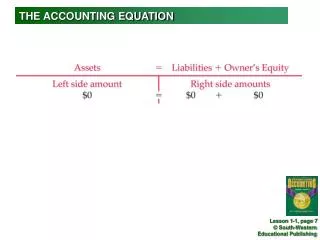

Solution 1: Below are the purposes of the accounting equation:- (i) Accounting equations despites the accuracy of a financial transaction. (ii) From accounting equations we can easily prepare final accounts. Question 2: Which of the following equations are correct? I. Assets = Capital + Liabilities II. Assets = Capital – Liabilities III. Assets = Liabilities – Capital IV. Capital = Assets – Liabilities V. Capital = Assets + Liabilities VI. Liabilities = Capital + Assets VII. Liabilities = Capital – Assets VIII. Liabilities = Assets – Capital Solution 2: The correct equations from the above equations:- I. Assets = Capital + Liabilities

IV. Capital = Assets – Liabilities VIII. Liabilities = Assets – Capital Hence, the correct equations are I, IV and VIII. Question 3: The position of a businessman on 30th June 1994 was as follows – Cash Rs. 5,000, Debtor Rs. 20,000, Machinery Rs. 60,000, Stock Rs. 25,000, Capital Rs. 75,000. Calculate his liabilities. Solution 3: It is given that Capital = Rs. 75,000 Calculation of Total Assets:- Total Assets = Cash + Debtors + Machinery + Stock Total Assets = Rs. 5,000 + Rs. 20,000 + Rs. 60,000 + Rs. 25,000 Total Assets = Rs. 1,10,000 Calculation of Liabilities:-

Liabilities = Assets - Capital Liabilities = Rs. 1,10,000 – Rs. 75,000 Liabilities = Rs. 35,000 Question 4: What entry (debit or credit) would you make to:- (a) Increase in revenue (b) Decrease in expense (c) Record drawing (d) Record the fresh capital introduced by owner Solution 4: (a) Credit – Increase in revenue (b) Credit – Decrease in expense (c) Debit in Capital Account – Record drawing (d) Credit in Capital Account – Record the fresh capital introduced by owner

Question 5: If a transaction has the effect of decreasing an asset, is the decrease recorded as a debit or credit? If the transaction has the effect of decreasing a liability, is the decrease recorded as a debit or credit? Solution 5: (i) Assets decrease will be the credit. (ii) Liability Decrease will be the debit. Question 6: Name the transaction that will (i) Decrease the assets and decrease the capital (ii) Increase the assets and increase the liabilities (iii) Increase the assets and decrease another asset (iv) Decrease the assets and decrease the liabilities Solution 6: (i) Decrease the assets and decrease the capital – Cash withdraw for personal use Drawings. (ii) Increase the assets and increase the liabilities – Purchase an asset on credit basis. (iii) Increase the assets and decrease another asset – Sale or purchases of stock on cash basis. (iv) Decrease the assets and decrease the liabilities – Paid amount to creditors.

Question 7: What will be the effect of the following on the accounting equation:- (i) Purchased goods for Rs. 20,000 form Mahesh on credit (ii) Sold goods to Suresh costing Rs. 8,000 for Rs. 10,000 in cash (iii) Paid wages Rs. 500 (iv) Withdrew in cash for private use Rs. 2,000 (v) Paid to creditors Rs. 2,000 Solution 7: (i) Stock Increases by Rs. 20,000 on assets and Creditors Increases by Rs. 20,000 on liabilities. (ii) Cash Increase by Rs. 10,000 on assets, Stock decrease by Rs. 8,000 on assets and Capital increase by Rs. 2,000. (iii) Cash Decrease by Rs. 500 on assets and Capital decrease by Rs. 500. (iv) Cash Decrease by Rs. 2,000 on assets and Capital decrease by Rs. 2,000. (v) Cash Decrease by Rs. 2,000 on assets and creditors decrease by Rs. 2,000 on liabilities. Question 8: If the total asset of a business is Rs. 2,00,000 and the net worth (capital) is Rs. 1,50,000. Calculate creditors.

Solution 8: Liabilities (Creditors) = Assets – Capital Creditors = Rs. 2,00,000 - Rs. 1,50,000 Creditors = Rs. 50,000 Therefore, the amount of creditors are Rs. 50,000. Question 9: A business on 1st April 2011 with a capital of Rs. 5,00,000. On 31st March 2012, his assets were worth Rs. 7,80,000 and liabilities Rs. 70,000. Find out his closing capital and profits earned during the year. Solution 9: Calculation of Closing Capital:- Closing Capital = Closing Assets - Closing liabilities Closing Capital = Rs. 7,80,000 – Rs. 70,000 Closing Capital = Rs. 7,10,000 Calculation of Profit:- Profit = Closing Capital – Opening Capital

Profit = Rs. 7,10,000 - Rs. 5,00,000 Profit = Rs. 2,10,000 Therefore, Profit of the firm is Rs. 2,10,000. Question 10: On which side will the increase in the following account be recorded? Also, mention the nature of the account. 1. Cash 2. Machinery 3. Debtor 4. Creditor 5. Proprietor’s Account 6. Rent Received 7. Salary Paid 8. Interest Received Solution 10: 1. Cash Nature of Account - Assets Side of the Account - Debit 2. Machinery Nature of Account - Asset Side of the Account – Debit 3. Debtors Nature of Account - Asset Side of the Account - Debit

4. Creditors Nature of Account - Liabilities Side of the Account – Credit 5. Proprietor’s Accounts Nature of Account - Capital Side of the Account – Credit 6. Rent Received Nature of Account - Income Side of the Account – Credit 7. Salary paid Nature of Account - Expenses Side of the Account – Debit 8. Interest Received Nature of Account - Income Side of the Account – Credit Question 11: On which side will the increase in the following account be recorded? Also, mention the nature of the account. 1. Furniture 2. Bank 3. Proprietor’s Account 4. Salary Paid 5. Salary Outstanding 6. Subash - A Customer Solution 11: S.no.-Particulars-Nature of Account-Side of the Account 1. Furniture Nature of Account - Assets Side of the Account – Debit

2. Bank-Assets-Credit Nature of Account - Assets Side of the Account – Debit 3. Proprietor’s Account-Capital-Debit Nature of Account - Capital Side of the Account – Debit 4. Salary Paid-Expenses-Credit Nature of Account - Expenses Side of the Account – Credit 5. Salary Outstanding Nature of Account - Liabilities Side of the Account – Debit 6. Subash Nature of Account – Customer (Assets) Side of the Account – Credit Download Free study materials for your Examinations at DKgoelSolution