Download

1 / 9

90 likes | 125 Views

DK Goel Solutions Chapter 8 Accountancy Company Accounts Issue of Debentures as per latest DK Goel Book available for free<br><br>https://dkgoelsolutions.com/class-12/chapter-8-company-accounts-issue-of-debentures/

E N D

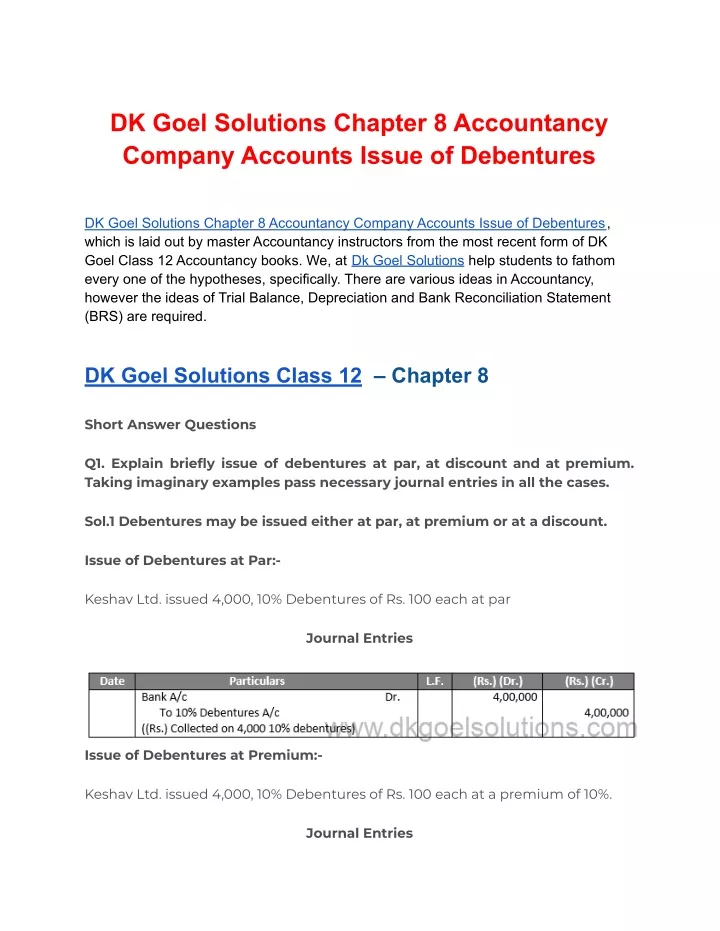

DK Goel Solutions Chapter 8 Accountancy Company Accounts Issue of Debentures DK Goel Solutions Chapter 8 Accountancy Company Accounts Issue of Debentures, which is laid out by master Accountancy instructors from the most recent form of DK Goel Class 12 Accountancy books. We, at Dk Goel Solutions help students to fathom every one of the hypotheses, specifically. There are various ideas in Accountancy, however the ideas of Trial Balance, Depreciation and Bank Reconciliation Statement (BRS) are required. DK Goel Solutions Class 12 – Chapter 8 Short Answer Questions Q1. Explain briefly issue of debentures at par, at discount and at premium. Taking imaginary examples pass necessary journal entries in all the cases. Sol.1 Debentures may be issued either at par, at premium or at a discount. Issue of Debentures at Par:- Keshav Ltd. issued 4,000, 10% Debentures of Rs. 100 each at par Journal Entries Issue of Debentures at Premium:- Keshav Ltd. issued 4,000, 10% Debentures of Rs. 100 each at a premium of 10%. Journal Entries

Issue of Debentures at Discount:- Keshav Ltd. issued 4,000, 10% Debentures of Rs. 100 each at a discount of 10%. The debentures are said to have been sold at a discount because the business offers debentures at a premium that is lee than their face or nominal value. A capital loss is a discount or loss on debenture issuance. It may be charged down by debiting the benefit or loss statement or the securities premium balance account. Journal Entries Q2. Can the debentures be issued for consideration other than cash? Give their journal entries. Sol.2 A business buys some properties from the seller and instead of paying the seller in cash, the company may opt to offer debentures to the seller in lieu of purchases. Such a dilemma of debentures to manufacturers for consideration other than cash is known as the question of debentures for debentures. Assets A/c Dr. To Vendors’ A/c (assets purchases)

Vendor’s A/c Dr. To Debentures A/c (issue of debenture to vendor at par) Vendor’s A/c Dr. To Debentures A/c To Securities Premium Reserve A/c (issue of debenture to vendor at premium) Vendor’s A/c Dr. Discount of issue of debenture A/c Dr. To Debentures A/c (issue of debenture to vendor at discount) Q3. Explain the meaning of debentures issued as collateral security. Sol.3 In addition to the principal protection, anytime a corporation takes a loan from a bank or any other party, the company will have to issue debentures as a subsidiary or secondary security. In addition to main security, collateral security means secondary security. In the company’s account books, there are two ways of dealing with such debentures:— 1. First Method:- No entry in the company’s accounts must be transferred in this manner, since the debentures are not officially released, but rather provided as collateral protection. As for the taking of a loan entry as passed only:—

2 Second Method:- In this process, with the entry for taking the loan, the entry for issuing debentures as collateral protection is also registered. Journal Entries Q4. What is the nature of debenture interest? Give journal entries to record. (a) When the interest is pending; and (b) When the interest is paid. Ignore tax. Sol.4 (a) When the interest is pending:- If a corporation pays half-yearly interest on debentures on 30 June and 31 December, while preparing the balance sheet on 31 March 2019, if the interest stays outstanding for the term ended 31 December 2018, it will be referred to as ‘interest accumulated and awaiting.’ (b) When the interest is paid:- If a corporation pays half-yearly interest on debentures on 30 June and 31 December, when preparing the balance sheet on 31 March 2018, the interest will be considered ‘Interest accumulated but not outstanding’ for the period from 1 January 2018 to 31 March 2018. i) When interest is pending:

Journal Entries ii) When interest is paid to the debenture holders: Journal Entries ii) On transfer of debenture interest to statement of profit and loss: Journal Entries Q5. What is meant by ‘debentures issued at par but redeemable at premium? Sol.5 The debentures are sold with the express condition that, at the point of their maturity, the corporation will pay a premium. While this premium will be charged at the time of eventual repayment, the Company reports those losses at the time of issue by debiting an account called “Loss on issuance of debentures A/c” since it is a known loss. Example:- If a debenture of Rs. 100 is issued at Rs. 100 and is redeemable at Rs. 105, the following entries will be passed: Entries For Issue: Q5. What is meant by ‘debentures issued at par but redeemable at premium?

Sol.5 The debentures are sold with the express condition that, at the point of their maturity, the corporation will pay a premium. While this premium will be charged at the time of eventual repayment, the Company reports those losses at the time of issue by debiting an account called “Loss on issuance of debentures A/c” since it is a known loss. Example:- If a debenture of Rs. 100 is issued at Rs. 100 and is redeemable at Rs. 105, the following entries will be passed: Entries For Issue: Entries For Redemption: Journal Entries Q6. What is meant by ‘debentures issued at discount and redeemable at premium’? Sol.6 If a debenture of Rs. 100 is issued at Rs. 98 and is redeemable at Rs. 105 the following entries will be passed:-

Entries For Issue: Journal Entries Entries For Redemption: Journal Entries Q7. What are the alternatives available to a company for the allotment of debentures when there is overs-subscription of debentures? Sol.7 Oversubscription of debentures suggests that the firm has collected more debenture applications than it has published. In such a case, any of the following three options or combinations can be assigned by the company: Rejecting excess queries, First Option. Second Option, distribution partial or pro-rata. A mixture of the above two options is the third alternative.

Q8. X Ltd. purchased assets of Rs. 8,40,000 and purchase consideration was paid by the issue of debentures at 5% Premium. Pass Journal entry. Sol.8 Journal Entries Download Free study materials for your Examinations