Download

1 / 5

50 likes | 62 Views

DK Goel Solutions for Class 12 Accountancy Chapter 7 Company Accounts Issue of Share as per latest DK Goel Book available for free<br><br>https://dkgoelsolutions.com/class-12/chapter-7-company-accounts-issue-of-share/

E N D

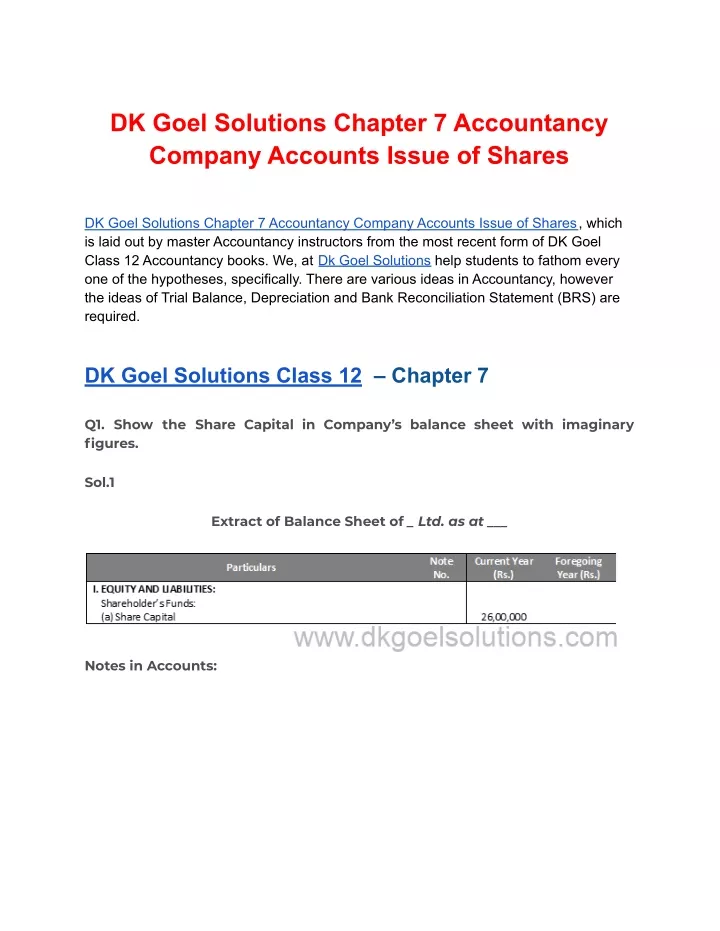

DK Goel Solutions Chapter 7 Accountancy Company Accounts Issue of Shares DK Goel Solutions Chapter 7 Accountancy Company Accounts Issue of Shares, which is laid out by master Accountancy instructors from the most recent form of DK Goel Class 12 Accountancy books. We, at Dk Goel Solutions help students to fathom every one of the hypotheses, specifically. There are various ideas in Accountancy, however the ideas of Trial Balance, Depreciation and Bank Reconciliation Statement (BRS) are required. DK Goel Solutions Class 12 – Chapter 7 Q1. Show the Share Capital in Company’s balance sheet with imaginary figures. Sol.1 Extract of Balance Sheet of _ Ltd. as at ___ Notes in Accounts:

Question 2. At least how much portion of the nominal (Rs.) of a share must be called as application money? Sol.2 At least 5 percent of share application money of the nominal value of shares. The money for the application must be deposited in a ‘Scheduled Fund’ by the corporation. Application money is a portion of the company’s equity capital and, as such, the application money is added to the share capital account as the directors assign the stock. Application funds raised by the organization when it shares are problems for the public. Question 3. What is the maximum Amount of a Call according to Table ‘F’ of Schedule I? Sol.3 The rules of table ‘F’ of Schedule I of the Companies Act, 2013 shall extend in the absence of the Articles of Association. The (Rs.) to be called up shall not exceed 25% of the complete quantity of the problem, either on application or on allotment or on any one call. Question 4. What is the minimum time interval between two consecutive calls according to Table ‘F’ of Schedule I? Sol.4

The rules of table ‘F’ of Schedule I of the Companies Act, 2013 shall extend in the absence of the Articles of Association. There must be an interval between making two calls for at least one month. Question 5. What journal entry shall you pass when shares are issued by a Public Limited Co. on premium? Sol.5 The sum of the securities premium can be paid on request or on allocation or also on calls by the Firm. Entries will be passed, if the Amount of premium is collected along with application money: If Amount of securities premium is collected along with allotment money.

Question 6. Can securities premium be utilised for the purchase of fixed assets? Give reason. Sol.6 No, the premium on shares cannot be used for the acquisition of fixed assets. Under Section 52(2) of the Companies Act, 2014, the (Rs.) of the Shares Prime can be used for the following purposes only: 1.) To pay down the company’s preliminary costs. 2.) To write off the costs, commission or discount permitted on the issuance of the company’s shares or debentures. 3.) In order to account for the premium owed upon redemption of the company’s redeemable preferred shares or debentures. 4.) For issuing incentive shares that are entirely charged. 5.) For the repurchase, as per section 68, of its own stock and other assets. Question 7. State any three purposes other than ‘issue of bonus shares’ for which securities premium can be utilized. Sol.7 Securities Premium should be used for:—

1.) To pay down the company’s preliminary costs. 2.) To write off the costs, commission or discount permitted on the issuance of the company’s shares or debentures. 3.) In order to account for the premium owed upon redemption of the company’s redeemable preferred shares or debentures. Download Free study materials for your Examinations at DK goel Solutions