Download

1 / 39

400 likes | 785 Views

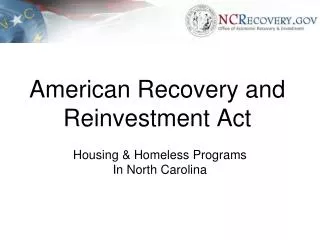

Preparation, Roles, & Responsibilities General Accounting Office May 7, 2009 American Recovery and Reinvestment Act Addressing State and Local Fiscal Challenges Through the American Recovery and Reinvestment Act April 2009 Federal Grants to State and Local Governments by Function

E N D

Preparation, Roles, & Responsibilities General Accounting Office May 7, 2009 American Recovery and Reinvestment Act

Addressing State and Local Fiscal Challenges Through the American Recovery and Reinvestment Act April 2009

Federal Grants to State and Local Governments by Function Source: Budget of the U.S. Government, Fiscal Year 2009, H. Doc. 110-84, Vol. III. Note: Data shown are 2007 Actual Outlays.

State and Local Governments Face Increasing Fiscal Challenges Percent of GDP Operating Surplus/Deficit Fall 2008 Operating Surplus/Deficit Jan 2009 Source: Historical data from National Income and Product Accounts. Historical data from 1980 – 2007, Sept. 2008 & January, 2009 GAO projections from 2008 – 2050 using many CBO projections and assumptions, particularly for next 10 years.

State and Local Fiscal Difficulties Are Largely Driven by Rising Health Costs Percent of GDP State and Local Government Non-Health Care Expenditures State and Local Government Health Care Expenditures Source: Historical data from National Income and Product Accounts. Historical data from 2000 – 2007, projections from 2008 – 2050. Note: Health care expenditures include health care benefits for employees and retirees and medical spending on behalf of individuals, such as Medicaid and SCHIP; Non-Health Care Expenditures include all expenditures with the exception of health care and interest payments.

State and Local Tax Receipts Would Have to Rise Well Above Projections under Current Law to Maintain Balance Taxes as a percent of GDP Maintain Balance Historical Growth Relative to GDP Base Case (current law) Source: Historical data from National Income and Product Accounts Note: Historical data from 2000 – 2007, projections from 2008 – 2050

The American Recovery and Reinvestment Act of 2009 (Recovery Act) • Has several provisions that may mitigate the fiscal difficulties that state and local governments are facing • Provides about $787 in spending and tax provisions: • Over $580 billion in additional spending • More than $275 billion in grants to states (including grants that go through states to individuals)

Purposes of the Recovery Act • To preserve and create jobs and promote economic recovery. • To assist those most impacted by the recession. • To provide investments needed to increase economic efficiency by spurring technological advances in science and health. • To invest in transportation, environmental protection, and other infrastructure that will provide long-term economic benefits. • To stabilize state and local government budgets, in order to minimize and avoid reductions in essential services.

Unique Requirements • Normally in Federal Contracts • New to Grants • Davis-Bacon Wages • Buy American

Recovery Act Emphasizes Accountability & Transparency • Enhanced Transparency • Normal Reporting to Federal Grantor Agency • Recovery.gov • Reporting • Federal Agency • State and Local Recipients • Individual Recipients

Entities Contributing to Reporting Requirements • Office of Management and Budget • Recovery Board • Federal Agency Inspectors General • Federal Agencies • Council of Economic Advisors • Congressional Budget Office • State and Local Auditors • State, Local, and Individual Recipients • GAO

Recovery Act Promotes Enhanced Oversight Role • Oversight • Recovery Board • GAO • Inspectors General • State and Local Auditors • Auditor General • State and Local Governments • Governor’s Office of Economic Recovery • General Accounting Office

Coordination of Oversight Activities • Coordination of oversight activities • GAO has developed a well-coordinated, non-duplicative, risk-based approach • Reached out to the Accountability Community and state associations • IG’s are best able to provide perspective of federal programs/agencies • GAO best positioned to give perspective of federal, state, and local governments’ use of funds • State auditors provide on-the-ground perspective

GAO’s Recovery Act Reporting Strategy 1. Bimonthly reports on State and local use of funds 2. Comment (with CBO) on quarterly recipient reports 3. Short-term reporting requirements, including: • Appointments to the Health Information Technology Policy Committee (due within 45 days of signing) • Small Business Administration’s efforts to increase liquidity in the secondary market for SBA loans (due within 60 days of signing) 4. Longer-term reporting requirements, including: • Current and past economic downturns since 1974 and make recommendations for addressing state needs during these periods (due April 2011)

GAO’s State and Local Reporting Strategy • Recovery Act requires GAO to “conduct bimonthly reviews and prepare reports on such reviews on the use by selected States and localities of funds made available in this Act.” • Strategy • Longitudinal study of 16 states and the District of Columbia • Selection criteria based on the stated purposes of the Recovery Act • Additional states added as other events dictate, including ongoing GAO work. • Localities sampled within selected states • GAO senior executives to coordinate with each selected state

Reporting Objectives • What improvements, if any, could be made to OMB's guidance to make it more clear and complete to states and local governments? • How are states and localities planning to spend Recovery Act funds and ensure that such spending is consistent with the stated purposes of the act? • What up front safeguards (i.e., before the money is spent), as well as ongoing monitoring, audits, and evaluations, do the selected states and localities have or are putting in place to guard against mismanagement and waste, fraud, and abuse? • What are the selected states and localities reported uses and plans to evaluate the impact of the funds they have received to date?

RecoveryAct Funds Using Tracking Safeguarding Assessing

Baseline information • • Amount of funds states received as of (date) by source & program • • Amount of funding disbursed or steps that are needed prior to disbursement • • How states will track funds received, how keep funds separate • • Any modification to accounting or reporting systems? Any cuff systems? • • Describe procedures and controls to help ensure accuracy • • Known weaknesses – single audits, program reviews, etc. • • Single Audit Results

Internal Control • • Internal control is an integral part of an organization’s management that provides reasonable assurance that the agency’s objectives are being met in the following categories: • - Effectiveness and efficiency • - Compliance with laws and regulations • - Safeguarding of assets • - Reliability of financial reporting • •Internal control helps managers achieve program results through effective stewardship of public resources— providing assurance that funds are used properly for their intended purposes. • •Internal control serves as the first line of defense in preventing fraud, waste, and abuse.

GAO Analysts’ Role The audit function is key to accountability of public programs and use of public funds. Obtaining an understanding of internal control is considered a basic audit requirement for financial and performance audits, in U.S. and international standards. Yellow Book has specific requirement for considering Internal control in the planning phase, when determining the objectives, scope and methodology for the job.

Control Environment • The Control environment • sets the tone for an organization, influencing staff awareness of good • controls, procedures, accountability, and program management. It is • the foundation for all other components of internal control, • providing discipline and structure. • Elements of the Control environment are: • Personal and professional integrity and ethical values of management and staff, including a supportive attitude toward doing things right • Commitment to competence • Tone at the top • Organizational structure • Human resources policies and practices

Control Environment • Relevant questions: • How is management dealing with competing demands-get the funding out fast while maintaining accountability? • Are sufficient, qualified personnel on board to handle the new program activities? • Is the current organizational structure sufficient and appropriate to implement the new responsibilities? What types of changes are needed? • How will the office handle coordination of oversight activities with stakeholders?

Control Environment • The following are indicators of risk that the agency or program may not have a strong control environment • Has recently undergone major change– e.g. new responsibilities, reorganization, cuts in funding, expansion of programs, changes in management • Management does not address indicators of problems. • Employees do not understand what behavior is acceptable or unacceptable, or are generally disgruntled. • Top management is unaware of actions taken at the lower level of the organization. • It is difficult to determine the organizations or individuals that control programs or particular parts of a program. • The organizational structure is inefficient or dysfunctional

Risk Assessment …is the identification and analysis of relevant risks from both external and internal sources that could negatively impact the organization’s ability to achieve program or agency objectives. …generally includes estimating the risk’s significance, assessing the likelihood of its occurrence, and deciding how to manage the risk and what actions should be taken. …is generally part of an overall strategic approach to management and is important for decisions on allocating resources and responsibility (accountability)

Risk Assessment • Relevant questions: • has the state used a risk based approach to identify strengths and vulnerabilities? • How are risks being mitigated? • Does ARRA funding present new or increased risks? • How will the state assess risks that subawardees won’t use ARRA funding appropriately?

Risk Assessment Red Flags include when the agency or program does not have: well-defined objectives adequate performance measures an adequate strategic plan

Control Activities • Control activities are the policies and procedures established to • achieve the entity’s objectives. They help ensure that management’s • directives are carried out in daily program operations. Examples of • control activities include • Authorization and approvals for transactions and other events. • Verifications and reconciliations. • Controls over access to assess, resources, and records. • Management-level reviews of program performance and other activities. • Documentation of transactions, approvals, and other significant management involvement in program activities. • Supervision, including assigning, reviewing work, training. • Development of formal policies and procedures to govern the above.

Control Activities • Relevant questions: • What control activities will help ensure that funding will be used for intended purposes? • What control activities are in place to minimize fraud, waste, and abuse? (eligibility of recipients, prescreening of grantees and contractors, oversight of use of funds by grantees and contractors) • Methods the state plans to use for competing grants and contracts • Excluded Parties List (suspended and disbarred business and individuals)

Control Activities Red Flags The agency or program has recently undergone major change– e.g. new responsibilities, reorganization, cuts in funding, expansion of programs, changes in management. Agency or program is understaffed and/or workload has drastically increased, and staff are having difficulties handling operational workload. There have been previous issues with fraud, waste, or abuse. Employees are unaware of policies and procedures, but do things the way “they have always been done.” Operating policies and procedures have not been developed or are outdated. Key documentation is often lacking or does not exist. Control environment is bad Employee morale is bad

Information and Communication Information is needed by management and employees to monitor program implementation while maintaining proper accountability and internal control. Pertinent information should be regularly tracked and communicated throughout the organization (down, up, and across) so that employees in all levels of the organization understand their role in achieving the organization’s mission and objectives, and their roles and responsibilities in maintaining proper internal controls.

Information and Communication • Relevant Questions • Is adequate written policies and guidance available to those who are implementing the program and monitoring uses of funds? • What type of program status and monitoring information will be distributed, who will be using it? • Has the state established financial reporting requirements on the use of ARRA funds? • What information does management use for decision making about program implementation, monitoring, and oversight? • How is the status of program implementation and any known risks and weaknesses communicated to those who are in a position to mitigate those risks?

Information and Communication Red Flags- When top management needs information, there is a mad scramble to assemble the information, or the process is handled through ad hoc mechanisms. Key information requests for basic information on the status of operations are difficult for the agency to respond to and require extra resources or special efforts. Management is using poor quality information or outdated information for making decisions. Staff are frustrated by requests for information because it is time consuming and difficult to provide the information. Management does not have reasonable assurance that the information it is using is accurate

Monitoring Internal control systems should be monitored to assess their effectiveness and to modify procedures as appropriate based on results of the monitoring activities (feedback). Monitoring is accomplished through routine, ongoing activities, separate evaluations, or both, and should be built into the normal, recurring operating activities of an entity. The monitoring process should also be used to ensure that audit findings and recommendations are adequately and promptly resolved.

Monitoring • Relevant questions: • How will the state monitor status of funds, and performance? How will this be linked with state goals? • What resources will be dedicated to monitoring Recovery Act funds and what opportunity costs are associated with this? • What types of oversight, onsite visits, and project inspections will be conducted for grantees and contractors?

Monitoring • Red Flags: • Significant problems exist in controls and management was not aware of those problems until a big problem occurred or until another outside party brought it to their attention (e.g. a recipient of funding, or an external audit). • The agency or program has recently undergone major change– e.g. new responsibilities, reorganization, cuts in funding, expansion of programs, changes in management. • There are problems with the other control elements: control environment, risk assessment, control activities, information and communications. • Previous audit findings are not being resolved adequately or timely. • Program is in general chaos.

Sub-Recipient Monitoring • Partnership for Intergovernmental Management and Accountability • New Guidance • Risk Assessment Monitoring Tool- http://www.agacgfm.org/intergovernmental/downloads/riskassessmentmonitoringtool.pdf • Financial and Administrative Monitoring Tool- http://www.agacgfm.org/intergovernmental/downloads/financialadministrativemonitoringtool.pdf

Arizona Specific • Coordinate with Governor’s Office of Economic Recovery • Coordinate with ADOA-GAO • GAO Policies: Current and Future • GAO Website: Required to Subscribe • Still Evolving: Watch for Developments • Communication (3 Basic Rules: Communicate, Communicate, Communicate) • Future Meetings

Agency Issues What can agencies do? • Coordinate with Governor’s Office & GAO • Who is the agency point person? • Who is responsible for oversight? Consider multiple perspectives: agency activity, sub-recipients, etc. • How do we plan to report? • What can our agency be doing now? • Stay Tuned! • Be flexible and ready to change!

Questions & Comments • What are your concerns? • How are you preparing? • What can we do to help? • Have you considered resource requirements? • Other?