Download

1 / 5

50 likes | 353 Views

90-10 Compliance Issues. B. ECASLA $2000: Expires 6-30-11 w/o Extension1. ECASLA $$: Part or all of extra $2000 beyond regular unsub loan amount, non-T4 treatment 2. Payment Period : actual disbursements in payment period (PP) compared to what would have been made w/o $2000 ECASLA unsub $$3. M

E N D

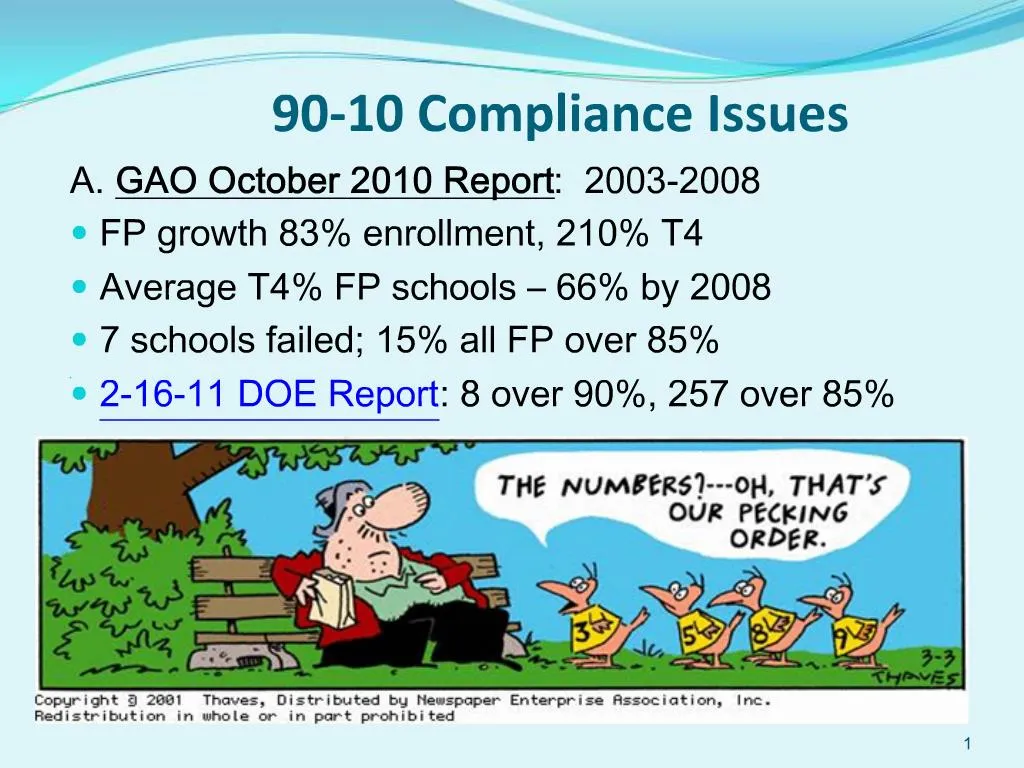

1. 90-10 Compliance Issues A. GAO October 2010 Report: 2003-2008

FP growth 83% enrollment, 210% T4

Average T4% FP schools � 66% by 2008

7 schools failed; 15% all FP over 85%

2-16-11 DOE Report: 8 over 90%, 257 over 85%

1

2. 90-10 Compliance Issues B. ECASLA $2000: Expires 6-30-11 w/o Extension

1. ECASLA $$: Part or all of extra $2000 beyond regular unsub loan amount, non-T4 treatment

2. Payment Period : actual disbursements in payment period (PP) compared to what would have been made w/o $2000 ECASLA unsub $$

3. Meeting 90/10 w/o ECASLA??

* Pro forma calculation

*Increase tuition to create �gap� not covered by T4 ?

*Increase institutional loans (grad forgiveness?)

2

3. 90-10 Compliance Issues C. Title IV Ineligible Program (length/type): revenue includible in 90-10 denominator if program:

(1) is licensed/approved by state licensing agency; OR

(2) is accredited by a DOE recognized agency; OR

(3) leads to industry recognized credential or prepares student for exam to obtain credential; OR

(4) provides state required update training (CEU) for maintaining licensure, OR

(5) provides specialized training for additional or advanced licensure within a vocational field.

4. 90-10 Compliance Issues D. Institutional Loans:

1. Period: 7/1/08 to 6/30/12

2. Loan � NOT installment payments under enrollment agreement or tuition billing plan

3. Need formal elements:

(A) Written enforceable promissory note: need fixed maturity; probably need to charge interest

(B) Loans made at regular enrollment intervals � not year end

(C) Regular loan repayments/collections (beware quick or high % write-offs)

4

5. 90-10 Compliance Issues E. Qualifying Institutional Scholarships (cash/discount)

1. Restricted special account maintained by institution

2. Published grant criteria focused on academic merit and/or financial need

* Written applications

* Written award letters

* Regular cycles � i.e., not year end

3. Funds in account must be from: (i) outside sources � not institution or affiliates (employees & shareholders), or (ii) income earned on such funds

5