Download

1 / 21

210 likes | 674 Views

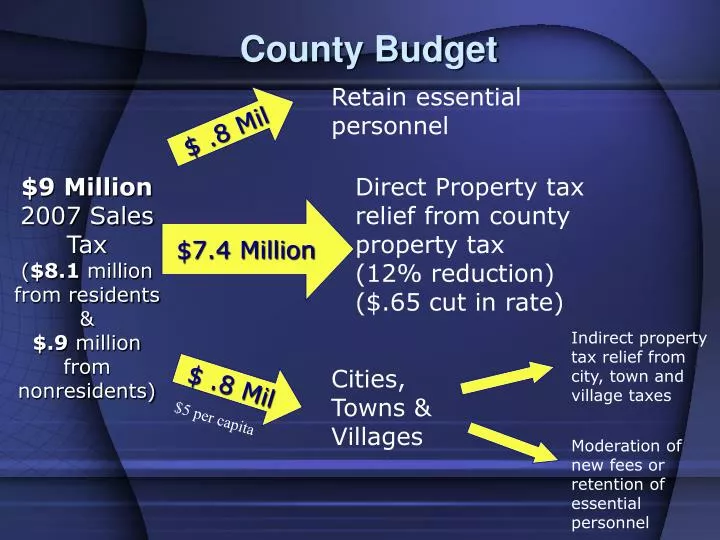

County Budget. Retain essential personnel. $ .8 Mil. $9 Million 2007 Sales Tax ( $8.1 million from residents & $.9 million from nonresidents). Direct Property tax relief from county property tax (12% reduction) ($.65 cut in rate). $7.4 Million.

E N D

County Budget Retain essential personnel $ .8 Mil $9 Million2007 Sales Tax($8.1 million from residents & $.9 million from nonresidents) Direct Property tax relief from county property tax(12% reduction)($.65 cut in rate) $7.4 Million Indirect property tax relief from city, town and village taxes $ .8 Mil Cities, Towns & Villages $5 per capita Moderation of new fees or retention of essential personnel

The average home in Winnebago County has grown in value to about $124,000. • That is a 3.8% increase from 1/1/05. • With the maximum equalized rate under the levy freeze, the average homeowner will see a $40increase on their County property tax from the prior bill • If the property tax relief/sales tax proposal is adopted, the average homeowner will see a $55decrease on their County property tax from the prior bill

To determine your individual benefit of the property tax relief/sales tax, you need to know how much your household spends on items subject to sales tax and the fair market value of your property. Remember that debt payments, groceries, medicine and most services are not subject to sales tax. Also note that the sales tax would not begin until April 1, 2007. Sales tax will vary widely from household to household but a rough average would be 43% of your Gross Income times .005 times 9/12. • EXAMPLE:$48,000 (total gross income) x .41 $19680 x .005 98.40 x .7573.80

The property tax savings can be estimated by taking the fair market value of your home divided by 1000 times .76 • Example:$124,000 fair market value/ 1,000 124x .7694.24

For most households, the property tax savings and sales tax will net out to small amounts. This means that a household with $4000/month gross income, with a home worth $124,000 might expect to pay $73.80 in county sales tax and to save $94.24 in property tax. $ 94.24 (Property Tax Relief)- $ 73.80 (Pay in County Sales Taxes)$ 20.44 Savings *Example based on median household income and median home price. Actual results will vary according to circumstance.

Homeowners on tight budgets such as retirees on fixed incomes, families with children in college, and people with large medical bills, will likely save money while others with large disposable incomes may pay more. • Property tax savings will start with your tax bill due in January, but sales tax will only occur as you make purchases subject to sales tax on or after April 1, 2007. • Renters are generally believed to pay property taxes through their rent which should rise less with property tax cut.

Year after year local property taxpayers have carried a larger share of county expenses. • Under state imposed levy rules, Winnebago county’s equalized tax rate will increase in 2007 unless a sales tax is adopted. Property tax relief is needed in 2007

How Do Property Taxes in Counties Without Sales Tax Compare to the State Average? • The 10 counties without a county sales or stadium tax have an average equalized property tax rate of $6.05. • The statewide average equalized property tax rate is $4.01.

How Do The Rates in Growth of the Property Tax Base Compare? • The growth in the property tax base in the ten counties without a sales tax averaged 6.84%. • The statewide average was 9.59%. • Each of the 10 counties w/o sales or stadium tax were below the average rate of fair market growth. • The relationship is probably not causal but clearly the sales tax does not harm growth in fair market value.

Tourism in Winnebago County • Winnebago County ranks 14th in tourism among Wisconsin’s 72 counties. • In 2005 tourists spent over $230 million in this county. • Winnebago county residents pay higher sales taxes when visiting 62 other Wisconsin counties than those county’s residents pay when they visit here.

Tourism in Winnebago County • More tourists visiting Wisconsin come from Minnesota and Illinois than any other states. • Illinois sales tax is 6.25%. • Minnesota’s sales tax is 6.5% (9% on alcoholic beverages and 16.2% on rental cars). • Tourists impact road maintenance, public safety, and sometimes the courts.

The last county to adopt a sales tax will have charged its residents more property taxes and provided them with less services for the benefit of tourists who will not even be aware that they are being favored at the expense of local residents.

Who Benefits Most From a Shift Between Property Taxes and Sales Tax? • Property owners with modest incomes, high medical expenses, or children in college. • Farmers who are often land rich and cash poor. • Manufacturers and their workers because materials and energy used in production are not subject to sales tax.

How Would Sales Tax Revenues Be Used? • 82% would be used for direct property tax relief. • 9% (tourist share) would be used to preserve essential County services. • 9% would be transferred to cities, villages, and towns on a per capita basis to preserve essential services, to hold down fees, or to give additional tax relief as their leaders think best.

Tourist Dollars • the amount of new revenue retained by the County will be roughly equal to the sales tax revenue from tourists. • The County will continue to reduce its workforce and bargain for smaller pay increases. • This will reduce the portion of County spending raised from property tax, reversing a long-term trend.

To keep faith with County taxpayers, the adoption of Property Tax Relief and a County Sales Tax must be accompanied by miserly control of County spending

Why Does the Sales Tax Need to Be Adopted Now? • Essential local services are at risk because of the levy freeze combined with the past thriftiness of area Government. • State Legislators continue to flirt with revenue limits that might cut off the sales tax option in the future. This will benefit visitors at a local property taxpayers expense.

With or without a sales tax, it is time for elected officials to bring ongoing revenues in line with ongoing expenses. Continued use of one-time solutions to structural budget imbalances will put the County’s future at risk.

Will Taxpayers Accept Property Tax Relief and a Sales Tax? • 59 counties have adopted a sales tax between 1986 and 2006. There is no serious movement in any of those counties to reverse that decision. • None of those counties have shared the revenue with cities, towns, or villages. *Note: 3 counties w/o sales tax have a stadium tax and some counties have both taxes)

In the 2006 budget 43 positions were eliminated and raises and benefits were reduced for all non-represented employees. The County Executive’s 2007 budget proposal will eliminate 19 more positions (most through attrition) and the budgeted wages assume much smaller raises will be negotiated in the new union contracts.

A balanced budget without the property tax relief/sales tax proposal will require additional spending cuts. $775,000 to stay within the levy freeze limits + $1,177,000 to avoid raising the equalized rate + $2,247,000 to hold county property tax bills to a zero increase for the average homeowner. $ 4,199,000 This is in additional cuts beyond those made in the proposed budget.