Download

1 / 17

170 likes | 500 Views

The Use of Treasury Securities Yield as Benchmark Interest Rates. Rosita P. Chang, Ph.D., CFA Professor of Finance College of Business Administration University of Hawaii Conference on Development of Indonesian Government Bond Market July 25-26, 2000.

E N D

The Use of Treasury Securities Yield as Benchmark Interest Rates Rosita P. Chang, Ph.D., CFA Professor of Finance College of Business Administration University of Hawaii Conference on Development of Indonesian Government Bond Market July 25-26, 2000

Importance of an Efficient Government Bond Market • to finance fiscal deficits and public expenditures • to provide instruments and markets for monetary policy implementation • to precede development of broad based financial markets: to create benchmark interest rates for pricing ofother financial assets and liabilities

Risk & Return Tradeoff (1950-1999) Return Small Company Stock Large Company Stock . Long-Term Corporate Bond T-bills KRF Long-Term Govt Bond Intermediate Govt Bond Risk

Determinants of Interest Rate • Production opportunities • Time preferences for consumption • Expected inflation • Risk

Basic Bond Equationk = k* + IP + DRP + LP + MRP where: k = Nominal interest rate on a debt security k* = Real risk-free rate IP = Inflation premium DRP = Default risk premium LP = Liquidity premium MRP = Maturity risk premium

= Real risk-free rate T-bond rate if no inflation = Inflation premium = Rate on Treasury securities = k* + IP k* IP kRF Real versus Risk-Free Rates

Historical Rates of Returns (1950-1999) • Inflation 4.25% • Treasury Bills 4.38% • Medium Term Gov’t 5.28% • Long Term Gov’t 5.34% • Long Term Corporate 5.52% • Large Company Stock 13.00% • Small Company Stock 15.92%

Premiums Added for Different Types of Debt Securities • Inflation: 4.25% • Treasury bills, kRF: real interest rate + inflation risk premium [4.38% vs 4.25%] • Long Term Treasury: maturity risk premium [5.28% vs 4.38%] • Long Term Corporate: default risk premium [5.52% vs 5.34%]

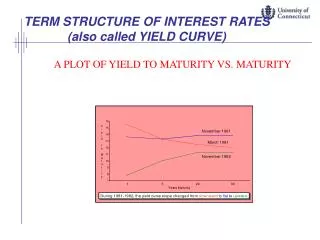

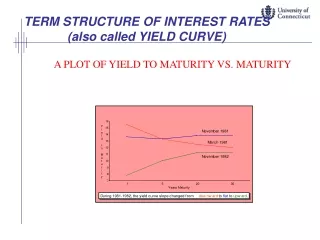

Usefulness of Government Bond Yields • Treasury securities yields are often used to describe term structure of interest rates and to chart yield curves • Term structure: the relationship between interest rates (or yields) and maturities • A graph of the term structure is called the yield curve

T-Bond Yield Curve Interest Rate (%) 1 yr = 6.11% 2 yr = 6.43% 5 yr = 6.29% 10 yr = 6.15% 30 yr = 5.19% 10 Yield Curve (June 2000) 5 Years to Maturity 0 10 20 30

Yield Curves on Different Types of Debt Instruments Interest Rate (%) 15 BB-Rated 10 AAA-Rated Treasury yield curve 6.4% 6.1% 5.5% 5 Years to maturity 0 0 1 5 10 15 20

Usefulness of the Yield Curve • To forecast interest rates • To select mis-priced securities in active bond portfolio management

Use of KRF inStock Valuation Models • The risk-free interest rate, kRF is also used as a basis for stock valuation models such as • Capital Asset Pricing Model (CAPM) • Arbitrage Pricing Model • Option Pricing Model

Use of KRF inCapital Asset Pricing Model (CAPM) • The Security Market Line (SML) is part of the CAPM which describes the relations between risk & return for individual stocks: • ki = risk-free rate + risk premium = kRF + (kM - kRF)bi

Use of KRF in Black-Scholes Option Pricing Model V = P[N(d1)] - Xe -kRFt[N(d2)] d1 = s t d2 = d1 - s t ln(P/X) + [kRF + (s2/2)]t

Government Securities as Effective Benchmarks • The government borrowing program should follow a regular and well publicized timetable • The government debt instruments should comprise of differing maturity => will ensure a complete range of benchmark yield curve that facilitates pricing of other financial instruments

Government Securities as Effective Benchmarks • There should be an active secondary government bond market • There should be a complete range of financial derivatives to complement spot trading of government bonds => will supply a critical mass of high quality security to the bond market enhancing investors’ awareness and confidence to debt securities