Download

1 / 10

100 likes | 103 Views

Consolidation of student loans is a means of merging several federal loans into one single, specific consolidation loan. By applying via the Federal Student Aid office of the U.S. Department of Education, borrowers can simplify the bill-paying procedure, reduce monthly loan payments, and find a repayment schedule that suits their needs. Consolidation may be used as an alternative to loan rehabilitation for borrowers who have defaulted on one or more federal student loans.

E N D

How to Consolidate Federal Student Loan Consolidation of student loans is a means of merging several federal loans into one single, specific consolidation loan. By applying via the Federal Student Aid office of the U.S. Department of Education, borrowers can simplify the bill-paying procedure, reduce monthly loan payments, and find a repayment schedule that suits their needs. Consolidation may be used as an alternative to loan rehabilitation for borrowers who have defaulted on one or more federal student loans.

Reasons for Loans Consolidation Overall, restructuring of student loans is only possible on federal loans. On the other hand, refinancing is open to both federal and private-loan borrowers. The consolidation can help to reduce and simplify monthly payments for borrowers with federal student loans. It is also a perfect way to obtain alternative repayment options and creditor rights, rehabilitate a defaulted debt, or even relieve debt repayment stress. Consolidation of student loans can be a reasonable choice if you plan to:

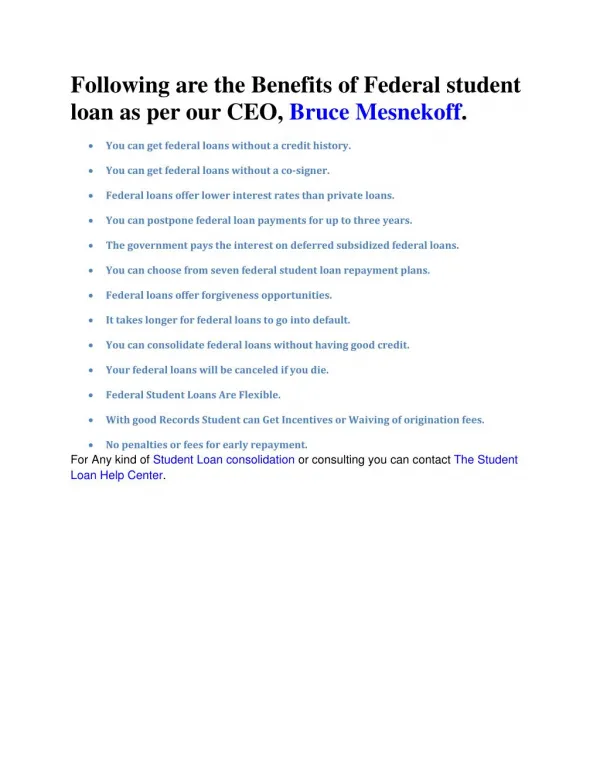

Reduced monthly payouts. Consolidation stretches the maturity period to 30 years and therefore reduces the monthly charge. Bear in mind that, in the long run, you will pay more interest on your loan. • Payments are made streamlined. If you are currently making payments to various servicers for student loans, consolidation will streamline this process so that you will only have to pay off one loan. • More repayment options and rights for borrowers. Federal loan consolidation enables borrowers to select from a variety of income-driven repayment options. Moreover, borrowers who may not otherwise qualify for the Public Service Loan Forgiveness will benefit by consolidating their federal student loans under a direct consolidation loan. • A separate servicer of loans. When you have issues with the existing federal student loan service provider, restructuring allows you the option to pick a new one. When you complete your application for consolidation, you will be asked to choose a servicer for the new loan.

An alternative to the rehabilitation of loans. When you still have student loans in default, credit consolidation will help you pay off the loan when you agree to repay the new loan with an income-driven repayment program or make three voluntary, on-time, and complete monthly payments on a defaulted loan before actually consolidating it. • Flat rates: The rate of interest on a Direct Consolidation Loan is a fixed rate of interest, meaning that it will remain the same for the duration of the loan. Unlike a private loan, the new federal fixed rate does not rely on current market trends but on the existing federal loans: the interest rate will be the weighted average of rates of interest on all your loans being combined, rounded to the nearest one-eighth of one percent. • Revived eligibility for benefits: According to finaid.org, if you merge your federal loans, it "resets the three-year clock on forbearance and deferments ." If you have used up your allocated deferment time before, including unemployment and economic hardship, you will now be eligible for them again. The same applies to forbearance, a provision that allows you to delay your student loan payments temporarily. •

Refinancing vs. ConsolidationThe consolidation of student loans allows borrowers to consolidate several federal student loans into one federal student loan only. Although consolidation streamlines multiple loans into one simplified payment, the amount of interest you pay over time will likely increase — saying that you can't save money via consolidation. The process then increases the repayment period, thus reducing the monthly payment but increasing the overall interest you must pay. In turn, student loan refinancing is the method of merging several private and/or federal student loans into one private loan. Unlike consolidation, refinancing helps lenders to reduce interest rates, which could save money over the loan 's lifespan. Refinancing student loans with a private loan does, however, mean that you do not have access to government loan protections, repayment plans, or forgiveness programs.

Pros of student loan consolidation • Prolonged repayment deadline • Simplified payment procedure • Lower monthly installments • Ability to change from a variable to a fixed-rate loan • Alternative strategies for repayment include phased and income-driven plans.

Cons of Student Loans Consolidation • The prolonged debt period means more interest payments over time. • Exceptional interest on specific loans becomes a portion of the consolidated loan principal. • Loss of consumer incentives on other loans, such as interest rate reductions, principal rebates, and cancelation incentives • You will lose credit for any pre-consolidation contributions to Public Service Loan Forgiveness or Refund Package. • You can't pay off single loans to reduce your monthly payment.

How to get approval for your Student Loans Consolidation Students who have left school, graduated, or dropped below half-time enrollment are qualified to consolidate their federal loans. There's no credit requirement for the consolidation of federal student loans. There are, however, several other conditions restricting who can apply for a direct consolidation loan:

Based on the type of loan, the loans you want to consolidate should already be in repayment or grace period, which lasts for six months after you graduate, leave school, graduate, or drop below half-time enrollment. • Generally speaking, if you have consolidated a loan already, you can not combine it again without merging another qualifying loan too. • Unless you make three straight monthly payments on the loan before consolidation or agree to repay your current direct consolidation loan under one of the income-related repayment programs, the loans you choose to merge can not be in default. • Similarly, consolidating a defaulted loan obtained by wage garnishment – or in compliance with a court order – is not permitted until the garnishment order is lifted or the judgment is vacated. • In contrast, refinancing of private student loans has close approval requirements to conventional loans. To qualify, lenders usually need a credit score in the upper 600s, a debt-to-income ratio below 50 percent, and a demonstrated potential to repay the loan.

007 Credit repair agent in Fullerton help increase your credit scores with guaranteed results. We audit your credit reports within minutes. Website: https://007creditagent.com/ Email: info@007creditagent.com Tel: (949) 258-7026 Address: 112 E. Amerige Avenue#109 Fullerton, CA 92832